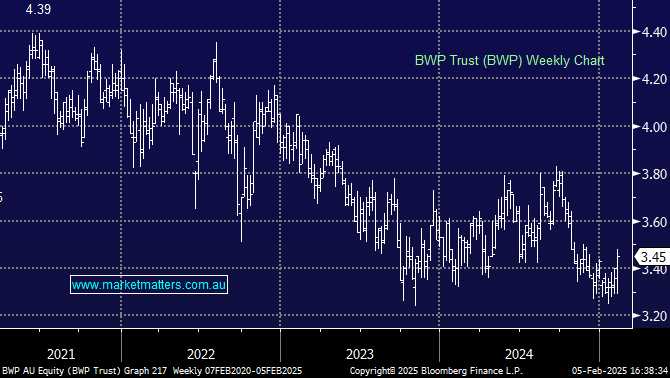

BWP +4.86%: A good/solid result from the predominately Bunnings Warehouse landlord, with rental growth feeding into higher distributions for this defensive REIT, that has been unloved;

1H25 underlying profit (excluding positive property revaluations) was $66.1m, up 15% YoY.

- Interim dividend of 9.20 cps, up 2.0% on this time last year.

- Guidance was for the same level of growth for the FY.

Occupancy is strong at 98.7% with a WALE of 4.4 years (up from 3.6 years). They achieved like-for-life rental growth of 3.3% along with positive revaluations across their book, which drove an uplift in NTA per unit to $3.92, up 4.8%. This means BWP is now trading at a ~13% discount to NTA when it has traditionally garnered a premium.

BWP is a high quality, defensive property company, yielding ~5.5% unfranked.

MM is bullish BWP following todays update

Add To Hit List