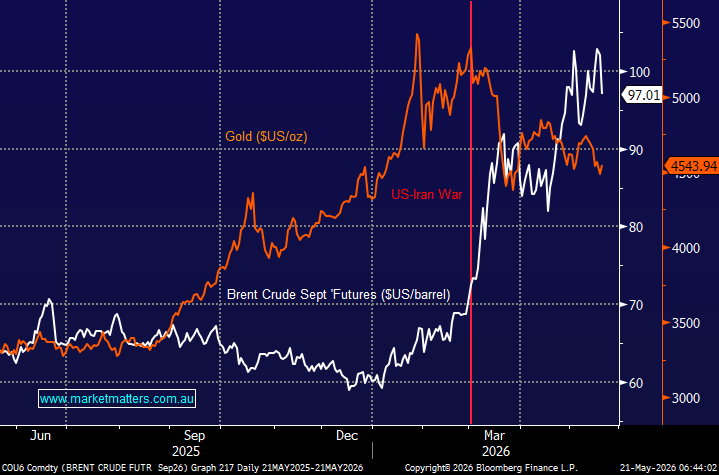

In yesterday’s webinar (recording available here) we were asked why the likes of gold were so weak of late. The answer is hopefully pretty clear in the chart below:

- Many investors expected gold to soar to fresh highs as the war broke out in late February, but instead it reversed lower.

The reasons were two-fold:

- Long gold had become a very crowded trade, leaving plenty of sellers, in to strength or weakness.

- As the oil price soared higher, bonds retreated, pushing up yields, reducing the relative appeal of precious metals after the “panic” like rally over the previous 6-12 months.

- The result was gold, and its related stocks/ETFs have been under pressure as the market priced in a greater chance of a rate hike, as opposed to cut rates.

Gold now needs a resolution to the Iran War and oil prices + bond yields meaningfully lower to regain its “Mojo.” The overnight ~5% drop in crude oil helped spark a $US60 bounce by the precious metal, but it’s the bond market that really needs to advance to see gold enjoy a meaningful resurgence.

- We believe an end to the conflict could be nigh, but it will take more than a knee-jerk reaction to see gold trade back towards/above $US5,000.

MM is cautiously bullish towards gold around $US4500/oz

Add To Hit List

chart

Brent Crude Sept’ Futures ($US/barrel) v Gold ($US/oz)

chart

Brent Crude Sept’ Futures ($US/barrel) v Gold ($US/oz)