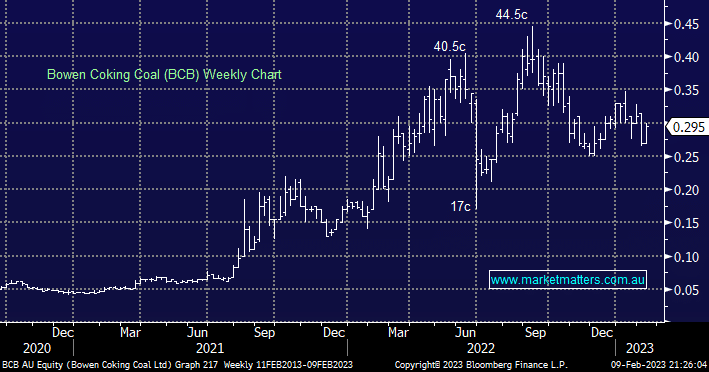

QLD based $541mn BCB is the junior player in the room, it doesn’t yet deliver bumper dividends/buybacks such as WHC & NHC. They have only recently announced their second shipment of ~40kt of metallurgical coal from its Bluff Coal mine and initial processing at Broadmeadow East, basically, this is a more aggressive/leveraged play than WHC/NHC towards higher coal prices for longer.

• We hold BCB in our Emerging Companies Portfolio, at this stage we are comfortable with our 4% exposure.

MM is bullish on BCB as a speculative play

Add To Hit List