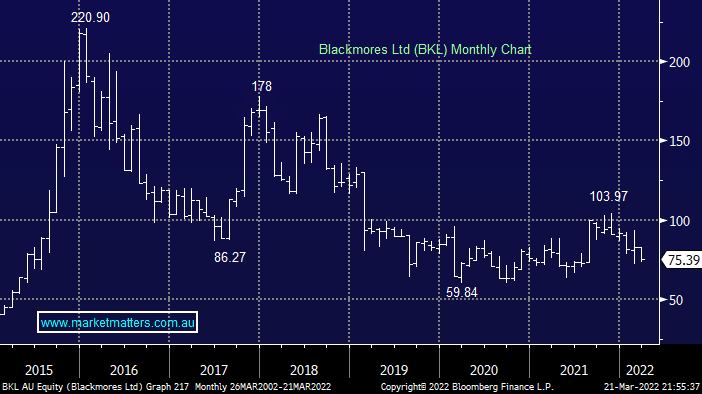

This is a great example of how a market favourite can fall from grace and just keep falling! MM hasn’t been a fan of BKL because of its Chinese dependency and increasing competition plus for good measure much of the worlds slowly moving away from tablet health towards simply healthy eating. However while the company does continue to deliver reasonable numbers, with the last half showing a 14.3% year on year lift in revenue, the stock should do “ok” but we believe at 47x 2022 earnings its simply too expensive in today’s environment and there’s better value elsewhere.

MM is neutral BKL at best

Add To Hit List