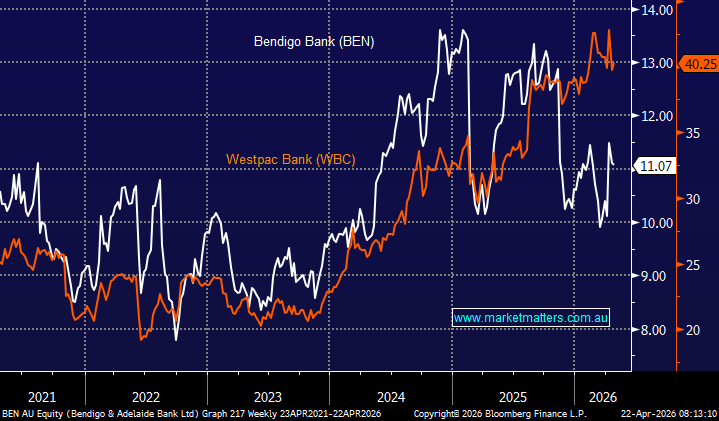

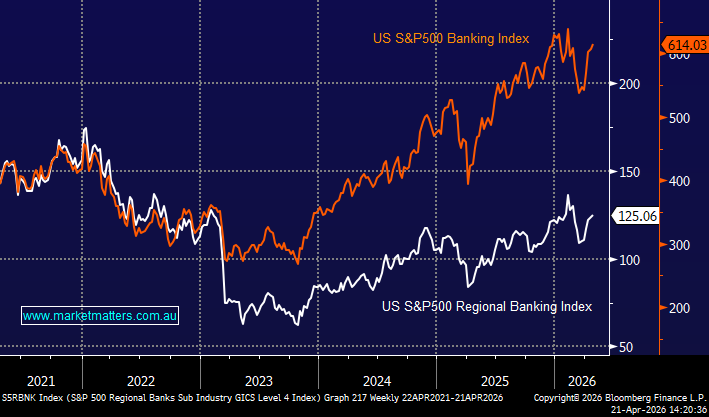

Is it time to reconsider the regional banks?

Bendigo & Adelaide Bank (ASX:BEN) delivered a stronger than expected 3Q26 trading update earlier this month, which has pushed the stock up ~12% so far in April, compared to the “Big Four”, which are struggling to hold up ~2%. BEN’s headline numbers were solid across the board: cash profits beat consensus by 12%, costs beat by 4%, the cost-to-income ratio improved to 60%, and net interest margin (NIM) expanded a welcome 6 basis points quarter on quarter (from a low base).

However, beyond the financials, the strategic news was arguably far more significant. BEN announced two new technology partnerships, one with Infosys covering IT services and AI-driven data automation, and a second with Genpact focused on professional services and agentic AI. For a regional bank carrying a structural scale disadvantage against the Big Four, these partnerships are very important. Technology is the most credible lever available to a bank of BEN’s size to close the efficiency gap, and management deserves credit for moving on this front. The associated restructuring carries a real price tag, $85–95 million in upfront transition costs, largely landing in FY27, but the run-rate expense benefit of $65–75 million by FY28 makes the maths extremely compelling.

The story, both locally and in the US, over recent years has been the major banks significantly outperforming the regionals, with the prohibitive costs to maintaining/evolving quality tech offerings pushing the disconnect. At home, CBA has been regarded as the best bank on many levels, including its tech stack: since the COVID lows, Australia’s biggest bank has soared ~330%, whereas BEN has struggled to double.

AI should help reduce the Big Four’s scale advantage over regional banks, but it won’t eliminate it. The democratisation of AI through affordable third-party partnerships means regional players like BEN can now access world-class capabilities in fraud detection, compliance automation and customer service for a lower cost.

However, the Big Four are not standing still, and their most durable advantage isn’t their spending power; it’s their data. AI systems improve with scale, and CBA’s 17 million customer dataset will always produce smarter models than a regional bank can build from a smaller base. The winners in this new landscape won’t be determined by who has the biggest technology budget, but by who deploys AI fastest and most effectively against the right problems, and for BEN, that’s precisely what the Infosys and Genpact partnerships are hoping to do.

- We think AI will help to close the gap between the regionals and “Big Four” banks.

Over the years BEN had walked a similar path to ANZ, until late 2025 since the arrival of Nuno Matos as CEO in May which has been welcomed with open arms by the market, pushing ANZ to new all-time highs in February. It’s also been a pretty similar path for Westpac. With AI improving BEN as an investment prospect, we question how it stacks up against ANZ and WBC, which we hold in the Active Growth Portfolio.

- ANZ Group (ASX:ANZ): ANZ’s rally since late 2025 is the combination of a new CEO with a credible plan, better-than-expected Suncorp synergies, a relatively attractive yield of ~4.6% part-franked (v peers), and the natural re-rating that comes when a deeply out-of-favour stock starts delivering against lowered expectations. The question for 2026 is whether the execution continues to match the rhetoric, and whether the regulatory clean-up can be completed without further unwelcome surprises.

- Westpac Banking Group (ASX:WBC): WBC has delivered strong returns in recent years, supported by a successful simplification strategy, a stronger balance sheet, and a broader re-rating of the majors as investors chased yield in a resilient domestic economy – the stock is forecast to yield ~4% fully franked. However, the recent pullback highlights the risk of that re-rating running too far too fast; trading at a premium to peers, and with its Q3 update flagging weaker market income and higher credit provisions, the market is now questioning whether a bank priced for perfection can sustain it.

- Bendigo & Adelaide Bank (ASX:BEN): BEN is getting ahead of the AI revolution and, as we looked at earlier, improving operationally. It’s forecast to yield ~5.7% fully franked, while it also trades on a lower valuation than all of the “Big Four” banks.

Not surprisingly, BEN offers the best yield and the cheapest valuation of the three, but there’s a reason for the discount. The restructuring story and technology partnerships are promising, but it lacks the scale, the earnings power, and the institutional investor following of ANZ and WBC. However, this lack of ownership could work in BEN’s favour – a little investor confidence can go a long way for an under-owned stock, similar to short-covering without the steroids.

However, BEN’s significant property exposure concentration is both its strength and its key vulnerability. In a rising property market, this is a tailwind, but in a downturn, a credit event, or a CGT-triggered selling wave, BEN has far less diversification to fall back on than either ANZ or Westpac. For investors assessing the May budget CGT risk, BEN’s loan book composition makes it the most directly exposed of the three to any deterioration in Australian residential property sentiment. Plus, MM believes AI will ultimately put many Australians out of work, which can only exert a negative impact on the local property market.

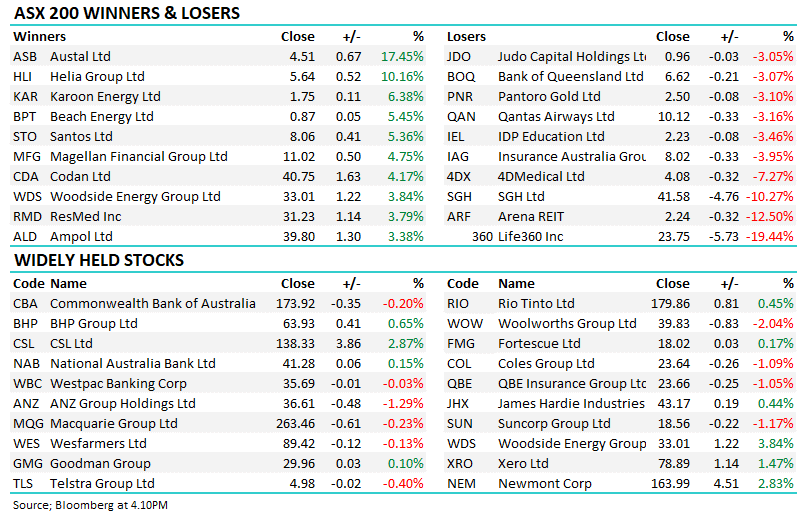

NB Fellow regional Bank of Queensland (ASX:BOQ) reports earnings today which will deliver another read through on the smaller end of the banking sector.

- We have considered BEN, for the first time in years, with a switch from Westpac an option, but on balance, it feels too early at this stage.