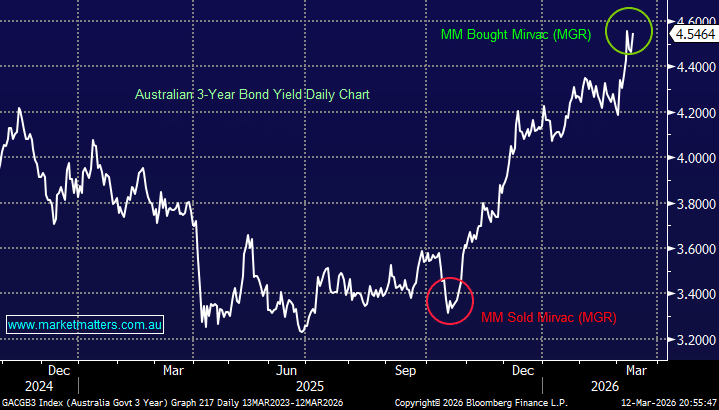

We sold MGR in late 2025 believing that it was “as good as it gets” for the doves with further rate cuts built into stocks, while in our opinion, the economic data was starting to paint a different picture. Now we have a surging oil price sparking inflation fears, weighing on bonds and pushing yields towards multi-year highs, but nobody is really giving much weight to the risks of an economic slowdown, apart from the aggressive selling of copper stocks. If growth slows, bond yields will ultimately decline as central banks adopt a more accommodative stance, i.e. this could now be “as bad as it gets” for bonds, hence we just bought back into MGR, a property stock which had retreated ~18% as bonds fell, sending yields higher.

- The local 3s appear to have at least 2 rate hikes built into their price, trading 0.65% above the current cash rate.

MM is neutral towards the 3-year yield ~4.5%

Add To Hit List