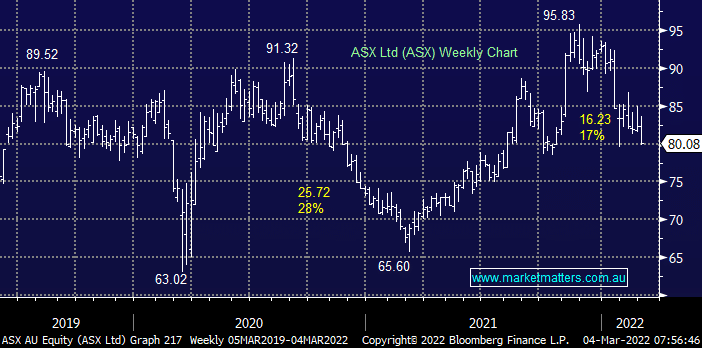

The ASX might be considered a relatively boring company compared to the 2 previous names but it’s catching our attention as it hovers 17% below November’s high while it’s an interesting defensive play in our opinion. The market didn’t react favorably to last month’s 1st half result which showed revenue up 6.6% to just over $500mn and NPAT up 3.5% to $250.3mn, the slight increase in dividend puts the stock on an estimated 12-month yield of 2.8% fully franked. The CEO is also stepping down at a time when the ASX is rolling out a huge project, replacing the CHESS system with a new clearing and settlement application. This seems a strange time to leave 12 months before the scheduled launch of such a huge update, with Australia being the first country globally to attempt such a feat.

The ASX is now trading on a forward P/E of ~29x, slightly above its longer-term average of ~28x but down from its recent peak of 36x, making it around about fair value. The ASX is ‘cheap’ on ~24x which would equate to a price sub ~$70.

With such a large project only 12 months or so from launch and a change of CEO, we would be more interested in ASX if it was nearer $70.

MM is neutral ASX around $80, and would be more interested nearer $70

Add To Hit List