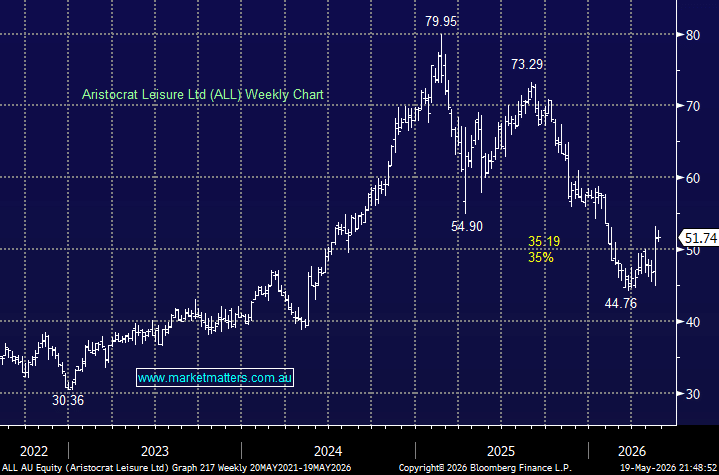

It’s been a tough year so far for Aristocrat Leisure (ALL) and Light & Wonder Inc (LNW), two of the world’s largest gaming technology companies, which both generate revenue from poker machines, digital casino content and online gaming platforms across global casino markets. Both stocks have been caught in the broader valuation reset across growth sectors, which has been particularly savage to companies where investors fear AI disruption could eventually threaten long-term earnings power. In early 2025, Aristocrat was soaring towards $80, enjoying a huge tailwind from the “certainty trade”, but similarly to the likes of Pro Medicus (ASX: PME) and JB Hi-Fi (ASX: JBH) its subsequently endured a sharp correction, trading from a valuation of 27x to sub 17x.

Last week, Aristocrat delivered a solid 1H result, which, importantly, wasn’t as bad as many feared, as we covered here. The stock rose nearly +14% on the day, as earnings and margins came in ahead of expectations, aided by continued market share gains in Gaming alongside a $1bn increase to the buyback program – meaningful for a $31bn business. The result prompted MM to consider if we’re currently “backing the wrong horse” in this space (given we hold LNW in the Growth Portfolio). Hence, today we’ve compared Aristocrat to Light & Wonder.

- Aristocrat’s revenue is flatlining in $A terms over recent halves between $3-3.3bn, but it’s the strong $A which is hiding the real story: Strip out FX and the business is growing at 6–7%.

The segment issue is Product Madness – it was once positioned as the high-growth digital engine. Social casino is a structurally challenged segment globally as players migrate to real-money gaming. For reference, Product Madness makes social casino games where players gamble with virtual chips rather than real money. As more US states legalise online gambling, players are increasingly shifting from “pretend” gaming to platforms where they can win actual cash—turning what was once a key digital growth engine into a growing headwind. People can increasingly download DraftKings or BetMGM and actually win cash, making paying $20 for fake chips start to feel pointless

- Product Madness is an issue weighing on Aristocrat; it’s close to 30% of its revenue that’s now under pressure as opposed to driving growth.

Aristocrat is effectively a three-speed business. Its core gaming machine division continues to deliver steady growth, Interactive is now the key long-term growth engine, and Product Madness remains in structural decline. The investment case now hinges on whether Interactive can scale quickly enough to offset the deterioration in social gaming, with the buyback giving management more time to execute on that transition.

- We believe Aristocrat is a solid business, but it’s hard to see it re-rating too fast on the upside with uncertainty across its different segments.

MM is cautiously bullish towards Aristocrat ~$52

Add To Hit List

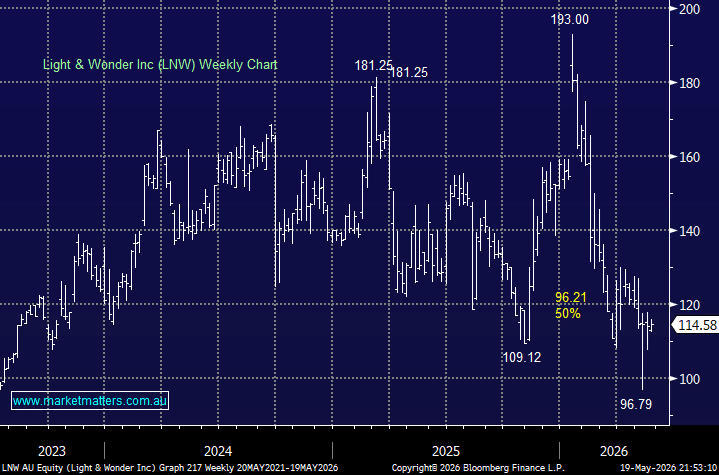

Moving onto Light & Wonder, its quarterly earlier in the month initially had the opposite reaction to ALL’s with the stock falling away but its subsequently recovered the ~10% drop. It was undoubtedly a softer-than-expected March quarter, with revenue and earnings missing consensus across its core Gaming and SciPlay divisions, although iGaming was a clear bright spot. Importantly, margins held up better than feared, cash flow remained solid, and management reiterated guidance for mid- to high-single-digit earnings growth in FY26, though the company continues to position FY26 as second-half weighted, as it did in FY25. There are a few moving parts with LNW that increase risk but also provide more upside:

Bullish Case: Their physical gaming machines hold a strong market share on casino floors globally. The iGaming division, providing content and platform technology to real-money online casinos, is growing into one of the most structurally attractive segments in global gaming as state-by-state legalisation accelerates across the US. The content library is deep, the technology platform is well regarded, and the recurring revenue streams are real. If debt is managed down, and earnings delivery follows over the next 12-18 months, the 65% gap between current price and analyst consensus should close fast.

Bear Case: This time last year, LNW borrowed $US800mn to complete the Grover acquisition. In other words, almost the entire acquisition was debt-funded – Grover Gaming operates electronic pull-tab machines in everyday community venues across several US states. LNW is now carrying over $US5bn in debt and needs to show the market it can successfully integrate last year’s acquisition, and continue to generate cash.

The risks around LNW are why it is trading noticeably cheaper than ALL; it is a more complex turnaround story, a genuinely good core business buried under a heavily leveraged balance sheet, questionable acquisition timing and resolved but costly litigation. However, the upside could be significant if management executes the deleveraging path, but the margin for error is relatively thin. If targets are met, the bullish rerating could be explosive – ALL may feel a safer bet today, but it’s LNW where we see the most upside.

- LNW has the potential to trade materially higher, but it is a riskier proposition – MM holds LNW in the Active Growth Portfolio.

MM is cautiously bullish towards Light & Wonder around $115

Add To Hit List