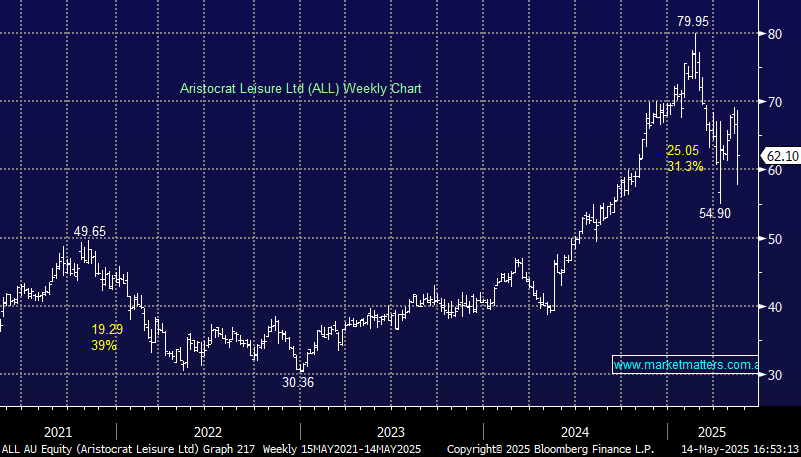

ALL -8.85%: Reported 1H25 results today that underwhelmed, driven by weakness in its gaming operations which saw revenue increase by a very lacklustre 2.4% for the year. Shares were down over 13% at their worst, which was an overreaction to a 9% miss at the earnings line, though clearly ALL is a very ‘owned’ stock.

- Underlying operating revenue of $3.03 billion, +8.7% y/y, relative to $3.3 billion consensus

- Adjusted NPAT of $732.6 million, was up +5.6% y/y but around $100m light on.

- Ebitda of $1.25bn was short of the $1.32bn expected.

- Interim dividend per share $0.44 vs. $0.360 y/y

The miss was driven by weakness in gaming and higher corporate costs. In terms of guidance, they expect to deliver profit growth over the full year to 30 September 2025 on a constant currency basis, and while vague, this is broadly what the market has factored in. We expect downgrades to numbers from analysts, but a decline into the low $60’s now presents a buying opportunity given the slight softness seems cyclical, not structural.

MM remains positive on ALL ~$60

Add To Hit List