APA makes money by owning and operating gas pipelines and energy infrastructure, earning stable, contracted revenue from customers that pay to transport gas. Most of its income comes from long-term “take-or-pay” agreements, which provide predictable cash flow regardless of usage levels. In simple terms, APA operates like a toll road for gas across Australia.

APA’s customers are primarily gas producers, electricity generators and energy retailers that rely on its pipeline network to move gas. This includes companies such as AGL and Origin, gas-fired power stations and large industrial users that require a secure supply. Most customers operate under long-term capacity contracts, providing APA with stable and predictable revenue – APA reports on Thursday.

For its regulated assets (such as gas distribution networks), returns are largely set by the Australian Energy Regulator, meaning pricing is determined through formal review processes rather than market forces. For its transmission pipelines, APA negotiates long-term contracts, but pricing is influenced by competition, contract renewals and regulatory oversight. In short, APA doesn’t have strong discretionary pricing power like a consumer brand — instead, it benefits from contracted, inflation-linked revenue streams that provide steady but capped returns.

Domestic gas consumption growth has been muted as Australia shifts toward renewables, putting pressure on pipeline utilisation and forecasts for long-term volume growth. So while not universal across Australia, it already is in Victoria, the trend is clearly toward gas-free new housing, which has longer-term implications for gas distribution demand. The shift is driven by emissions targets, electrification of appliances (heat pumps, induction cooktops) and the growing availability of rooftop solar and batteries. Moving forward, APA can still make money in a gas-free housing future, but it becomes more reliant on industrial demand, power generation and energy transition projects rather than household growth.

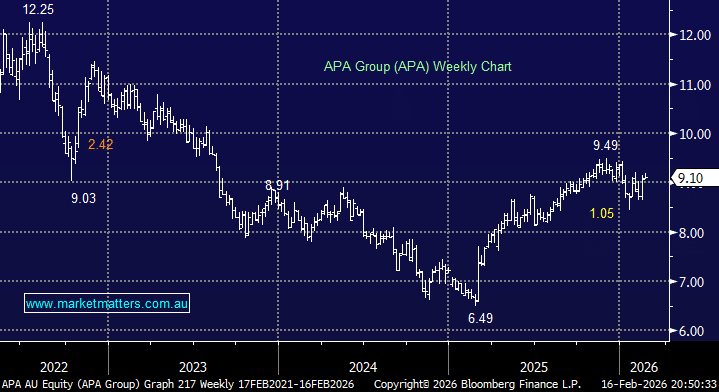

- We like APA for its more than 6% yield, but it’s not a stock set to benefit from AI energy demands: MM owns APA in its Active Growth Portfolio and Active Income Portfolios