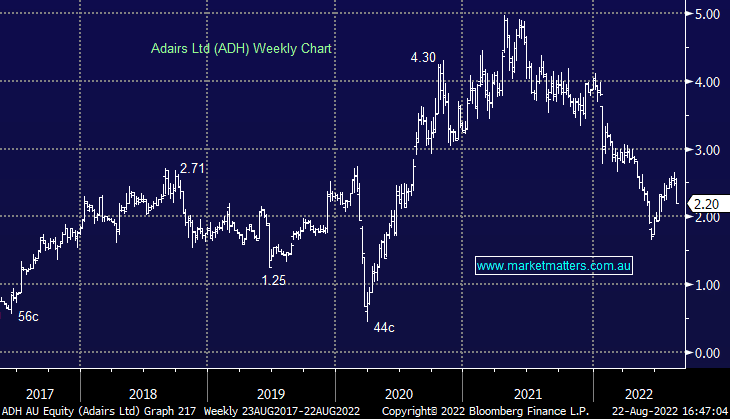

ADH -13.73%: the homewares retailer posted a disappointing FY22 result today, and soft guidance for the year ahead further weighed on shares. Revenue was in line, however, EBIT and Net Profit missed consensus by around 3%. Costs were higher in the period due to COVID lockdowns, supply chain issues and additional investments meant that profit fell ~30% despite sales growth of 13%. Most of the increase in costs will roll off for FY23, however, guidance was also below expectations. The market was slightly above the $75-85m EBIT guidance the company provided for the current period.

MM prefers LOV in the retail space

Add To Hit List