Market finishes up for the month

The market was a prism of strength today despite closing pretty much flat after a very weak open courtesy of selling primarily amongst the commodity stocks, however banks were also targeted post open – before buyers stepped into the fray from lunchtime onwards. The index continues to push up against recent highs however we remain on the sell side in aggregate at current levels, thinking that a combination of options expiry (yesterday), and end of month today could have provided some synthetic support for the main index driving stocks higher like the banks.

Today we made the (no doubt) controversial call to sell our holding Commonwealth Bank (CBA) however we also up weighted our position in BHP by another 2.5%. Selling strength and buying weakness is clearly one of the metrics we’ve spoken about often in recent times and today was an example of just that. More on the portfolio amendments below.

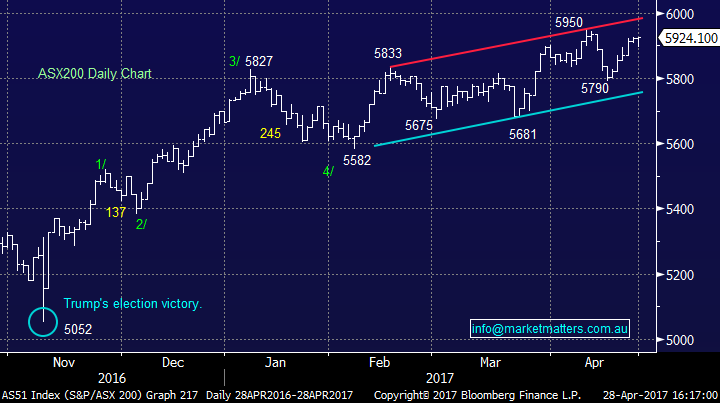

On the broader market today, we had reasonable range of +/- 30 points, a high of 5950, a low of 5894 and a close of 5924, up +2pts or +0.04%. For the month of April the market finished up +1.01% which is clearly positive, however underwhelming in terms of average April performance.

ASX 200 Intra-Day Chart

ASX 200 Daily Chart

Commonwealth Bank (CBA) – we took a +20% profit in CBA today which is one of those difficult calls to make. There’s no other stock on the ASX that polarises investors as much as CBA, although it’s worth noting that Telstra used to be like that as well! We’re not negative the banks yet, however given seasonal weakness in May and recent strength + optimism now obvious in the banks, we thought it prudent to reduce our exposure by 5.5%, and increase our cash levels overall. We still hold CYB, NAB and ANZ as direct banking exposure plus a number of other financials.

Commonwealth Bank (CBA) Daily Chart

We also added to our position in BHP today, adding to our existing 5% holding which we acquired just under $24. Today BHP opened down 2% around $24.40 and we were buyers, and it was pleasing to see the stock rally from the lows back to $23.72. We remain medium-term bullish the stock, believing it to be undervalued within both the sector and market. The stock is currently paying a 3% fully franked yield with the potential for positive buybacks in the near future as the stock evolves into a "cash cow".

BHP Billiton (BHP) Daily Chart

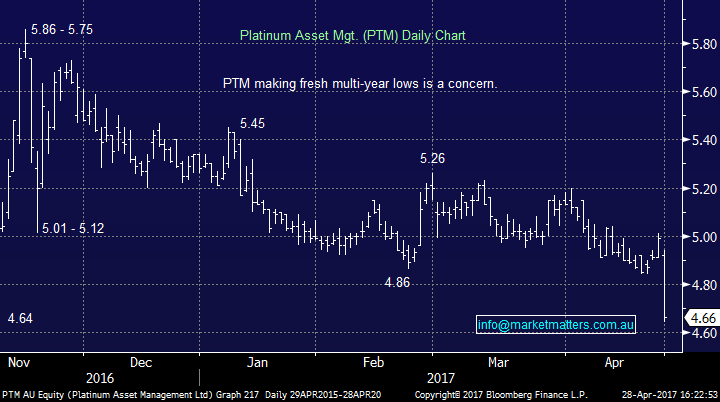

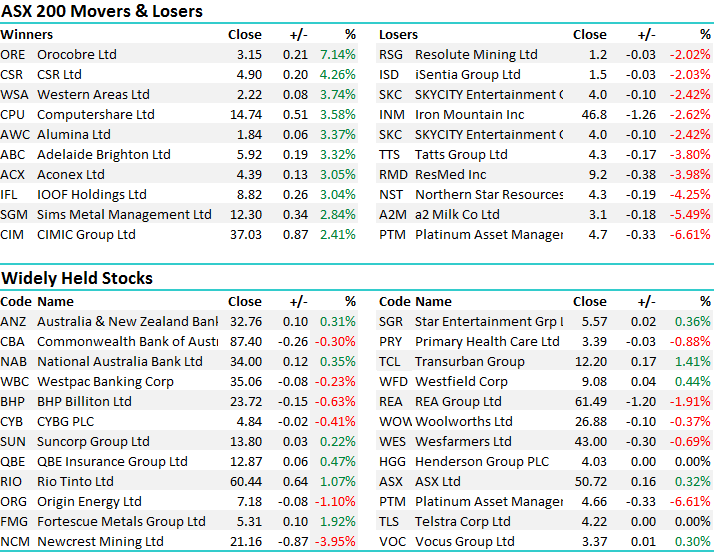

On the flip side, Platinum Asset Management (PTM) was weak today, dropping by -6.61% to close at $4.66. This is a stock that was very strong yesterday and started to look good technically, but dropped off the perch today. They announced plans to lower their fee structures which is clearly a reaction to competitive pressures. This is a negative to earnings, however only in so far as it’s not offset by an increase in FUM flow. Lower fees on more FUM is neutral however lower fees on the same FUM is negative. At this stage, the mkt pricing the later and the stock subsequently drops. There is a buy back in place that can be used, and we hope it is however the stocks clearly looks negative on the charts. One we will cover further in the weekend report tomorrow.

Platinum Asset Management (PTM)

Have a great night, and watch out for the Weekend report on Sunday

The Market Matters Team

Disclosure

Market Matters may hold stocks mentioned in this report. Subscribers can view a full list of holdings on the website by clicking here. Positions are updated each Friday.

Disclaimer

All figures contained from sources believed to be accurate. Market Matters does not make any representation of warranty as to the accuracy of the figures and disclaims any liability resulting from any inaccuracy. Prices as at 28/04/2017. 5.00PM.

Reports and other documents published on this website and email (‘Reports’) are authored by Market Matters and the reports represent the views of Market Matters. The MarketMatters Report is based on technical analysis of companies, commodities and the market in general. Technical analysis focuses on interpreting charts and other data to determine what the market sentiment about a particular financial product is, or will be. Unlike fundamental analysis, it does not involve a detailed review of the company’s financial position.

The Reports contain general, as opposed to personal, advice. That means they are prepared for multiple distributions without consideration of your investment objectives, financial situation and needs (‘Personal Circumstances’). Accordingly, any advice given is not a recommendation that a particular course of action is suitable for you and the advice is therefore not to be acted on as investment advice. You must assess whether or not any advice is appropriate for your Personal Circumstances before making any investment decisions. You can either make this assessment yourself, or if you require a personal recommendation, you can seek the assistance of a financial advisor. Market Matters or its author(s) accepts no responsibility for any losses or damages resulting from decisions made from or because of information within this publication. Investing and trading in financial products are always risky, so you should do your own research before buying or selling a financial product.

The Reports are published by Market Matters in good faith based on the facts known to it at the time of their preparation and do not purport to contain all relevant information with respect to the financial products to which they relate. Although the Reports are based on information obtained from sources believed to be reliable, Market Matters does not make any representation or warranty that they are accurate, complete or up to date and Market Matters accepts no obligation to correct or update the information or opinions in the Reports.

If you rely on a Report, you do so at your own risk. Any projections are estimates only and may not be realised in the future. Except to the extent that liability under any law cannot be excluded, Market Matters disclaims liability for all loss or damage arising as a result of any opinion, advice, recommendation, representation or information expressly or impliedly published in or in relation to this report notwithstanding any error or omission including negligence.

To unsubscribe. Click Here