Iron Ore tumbles (DLX, BHP)

WHAT MATTERED TODAY

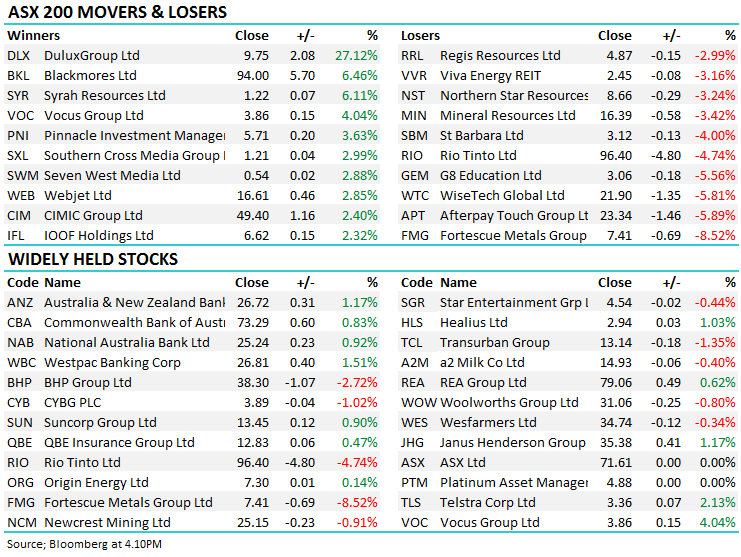

Surprisingly resilient day was seen on the local market today, once again held up by the banks. Resources took a hit though with the iron ore names finally coming off substantially all on the back of some better news from Vale. For those that missed it, Vale got the go ahead to resume use of one of the dams that the Brazil courts had placed an injunction over – the result is some supply will come back online shortly, although a number of dams still remain out of action as this Brazil disaster continues to play out. Fortescue (FMG) was hit the hardest as a result, falling 8.52%.

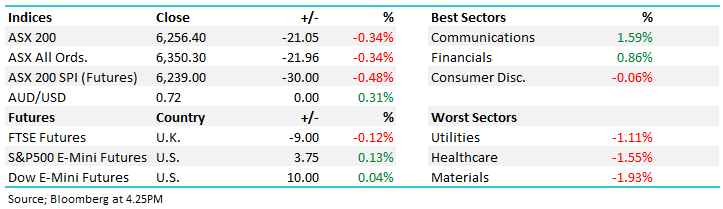

Overall today, the ASX 200 down -21 points or -0.33% at 6256. Dow Futures are trading higher, up +10pts / 0.04%

ASX 200 Chart

ASX 200 Chart

CATCHING OUR EYE;

DuluxGroup (DLX), +27.12%, shares traded strongly higher after the company confirmed it had received a takeover offer from Japanese company Nippon. The offer at $9.80/share was worth a 27.8% premium to yesterday’s close, with the stock traded through that level early in the session to a high of $9.87. The bid includes a fully franked dividend component and hence is worth more than $9.80 to many shareholders that are able to use the credits.

The board has unanimously recommended the bid, saying “it provides an opportunity for shareholders to realise a significant premium to market value and is on terms that reflect the strategic value of DuluxGroup.”

DuluxGroup (DLX) Chart

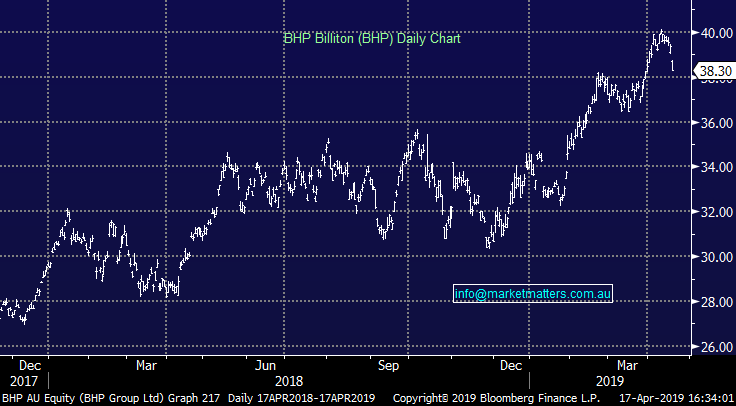

BHP (BHP), -2.72%, sold off today on the back of soft iron ore price movements, but held up better than its peers thanks to a reasonable quarterly production report. Similar to Rio Tinto’s report yesterday, BHP lowered iron ore guidance on the back the cyclone impact, however the rest of the production deck remained intact. One interesting thing to note was commentary around cost pressures on labour and energy however nothing to be overly concerned with just yet. As we have said before, iron ore price will remain choppy as this Brazil situation plays out and will present buying opportunities.

BHP (BHP) Chart

Broker Moves:

· Mirvac Group Downgraded to Hold at Deutsche Bank

· Mirvac Group Downgraded to Hold at Shaw and Partners; PT A$2.64

· Scentre Group Downgraded to Sell at Deutsche Bank

· Regis Resources Raised to Buy at Blue Ocean; Price Target A$6.30

· Telstra Upgraded to Buy at UBS; PT A$3.60

· Restaurant Brands NZ Cut to Underperform at First NZ Capital

· Cochlear Upgraded to Buy at Goldman; PT A$197

· Transurban Cut to Underperform at Credit Suisse; PT A$12.20

OUR CALLS

No changes to either portfolio today.

Have a great night

Harry & the Market Matters Team

Disclosure

Market Matters may hold stocks mentioned in this report. Subscribers can view a full list of holdings on the website by clicking here. Positions are updated each Friday, or after the session when positions are traded.

Disclaimer

All figures contained from sources believed to be accurate. Market Matters does not make any representation of warranty as to the accuracy of the figures and disclaims any liability resulting from any inaccuracy. Prices as at 17/04/2019

Reports and other documents published on this website and email (‘Reports’) are authored by Market Matters and the reports represent the views of Market Matters. The MarketMatters Report is based on technical analysis of companies, commodities and the market in general. Technical analysis focuses on interpreting charts and other data to determine what the market sentiment about a particular financial product is, or will be. Unlike fundamental analysis, it does not involve a detailed review of the company’s financial position.

The Reports contain general, as opposed to personal, advice. That means they are prepared for multiple distributions without consideration of your investment objectives, financial situation and needs (‘Personal Circumstances’). Accordingly, any advice given is not a recommendation that a particular course of action is suitable for you and the advice is therefore not to be acted on as investment advice. You must assess whether or not any advice is appropriate for your Personal Circumstances before making any investment decisions. You can either make this assessment yourself, or if you require a personal recommendation, you can seek the assistance of a financial advisor. Market Matters or its author(s) accepts no responsibility for any losses or damages resulting from decisions made from or because of information within this publication. Investing and trading in financial products are always risky, so you should do your own research before buying or selling a financial product.

The Reports are published by Market Matters in good faith based on the facts known to it at the time of their preparation and do not purport to contain all relevant information with respect to the financial products to which they relate. Although the Reports are based on information obtained from sources believed to be reliable, Market Matters does not make any representation or warranty that they are accurate, complete or up to date and Market Matters accepts no obligation to correct or update the information or opinions in the Reports. Market Matters may publish content sourced from external content providers.

If you rely on a Report, you do so at your own risk. Past performance is not an indication of future performance. Any projections are estimates only and may not be realised in the future. Except to the extent that liability under any law cannot be excluded, Market Matters disclaims liability for all loss or damage arising as a result of any opinion, advice, recommendation, representation or information expressly or impliedly published in or in relation to this report notwithstanding any error or omission including negligence.