Overseas Wednesday – International Equities & Global Macro Portfolio (WHC, LLOY LN, TTD US, IEM)

I’m off to Adelaide today in preparation for this weekends “Apex Outback Postie Bike Ride”, 4 days, off road through the Flinders Ranges on Honda CT110 ‘s. Currently we have raised over $13,000 – click here if you would like to help the cause.

Please note that reports will be shorter through the rest of the week and there will be no weekend report. We will be back again on Monday

The ASX200 is again knocking on the 6200 door, rallying over 1% on Tuesday to close at a fresh post March high. The buying was pretty broad based with only the Materials Sector closing in the red while the “Big Four” banks remained well bid all outperforming the index. While a few stocks did experience a little profit taking the underlying tone was clearly strong and the bears must be wondering what can stop this stimulus propelled juggernaut. My “Gut Feel” is the market is due a rest, at least for a few sessions, but the surprises are still likely to be in the direction of the trend which since March is clearly up.

The fuel for yesterday’s rally switched from growth to yield as buying rolled through almost all areas where investors usually search for dividends. It’s now only a few weeks until the next RBA meeting where official rates are expected to be cut from 0.25% to 0.1%, the bond market has the easing priced in as almost inevitable. With term deposits heading down below 0.5% it’s not surprising that yield hungry investors are chasing the reliable dividend payers. However, I caution subscribers that investors have in the past created a number of major tops through their indiscriminate hunt for yield, its one of our jobs moving forward to decide when enough is enough with this thematic.

MM remains bullish the ASX200 into Christmas.

ASX200 Index Chart

Yesterday the news was a buzz with the story that China had curbed the imports of Australian coal, this might be another political game or it’s another step by the world’s second largest economy to protect local jobs and progress towards clean energy. China has previously been comfortable spending many extra millions buying domestic goods as opposed to cheaper imports as they work on the internals of their domestic economy. China currently imposes an annual volume limit of coal for Australian miners and the current move could simply be to offset China’s mines being closed aggressively early in 2020 due to COVID, or of course something more sinister may be brewing.

Some might have been surprised to see Whitehaven (WHC) close up yesterday but in FY20 China was less than 2% of the companies revenue with Japan, Taiwan and Korea are far more important markets. If China doesn’t buy Australian coal its definitely not good news for any local players whether directly or indirectly, let’s hope that 2020’s quota of imported coal has been reached and the tap simply switched off until 2021. From a price perspective surprises do have a habit of unfolding with the trend and WHC is clearly bearish hence we believe any accumulation should only be considered into weakness.

MM likes WHC as “trade” around 80c but note we are unlikely to participate.

Whitehaven Coal (WHC) Chart

Overseas markets

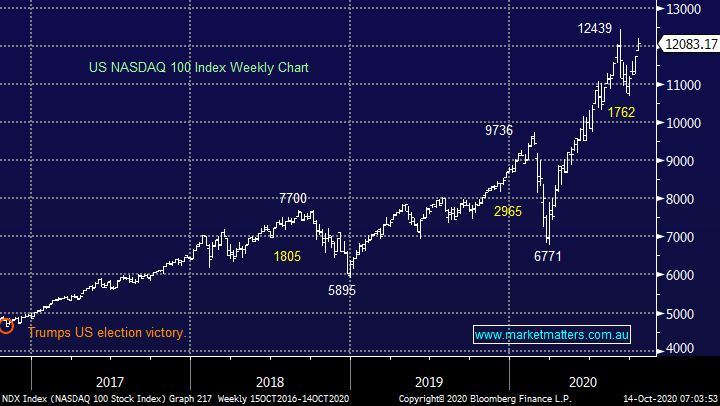

Overnight US stocks felt tired which is no surprise after their recent strong recovery to re-test all-time highs although the tech-based NASDAQ remains firm, even while the broader market “wobbles”. The technical picture for the IT Sector points to some choppy price action around current levels before a push above 13,000 i.e. buying pullbacks still feels the best opus operandum.

MM remains bullish US stocks into Christmas.

US NASDAQ Index Chart

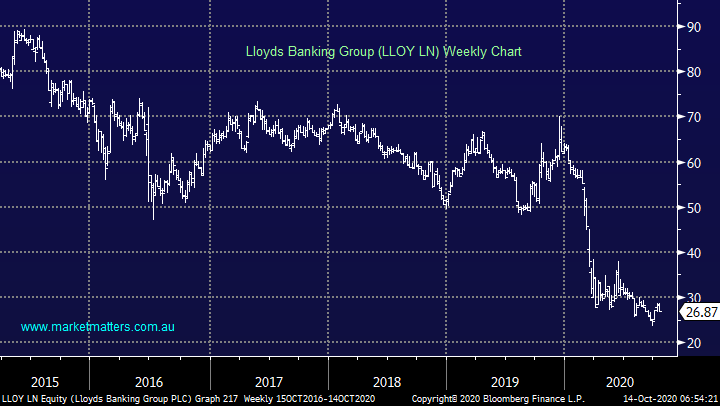

Overnight the Bank of England asked UK banks how ready they are for negative interest rates, a seismic step in monetary policy which theoretically is a huge headwind for the Banking Sector. Personally, I cannot imagine their banks haven’t already considered this possibility as official rates already sit at 0.1%. At least this shows a readiness for their central bank to do whatever is necessary to stimulate their post COVID economy which should help negate potential bad debts within the sector. We believe the lack of major sell off by the UK banks is very encouraging, MM feels the UK Banks are “looking for a low”.

MM is bullish UK banks at current levels.

UK FTSE Banking Index Chart

MM International Portfolio

No change to our positions / cash holdings this week, MM continues to hold only 6% cash in the MM International Portfolio : https://www.marketmatters.com.au/new-international-portfolio/

Boring I’m afraid but we continue to believe it’s still time to sit back and monitor our positions / market stance, we are long and skewed towards tech, reflecting our short-term view on the market but obviously we can be wrong hence the ongoing evaluation. If / when we see a strong move through October into Christmas MM is expecting a further couple of tweaks, out of tech into cash / financials / energy etc but there’s lots of twists in the road ahead before we hope / expect to be particularly active.

Over the last few weeks we’ve already witnessed a few sessions where there’s been pronounced rotation into cyclical laggards, a trend we can see this following through into 2021 i.e. the direction we expect to tweak towards in the coming months. Following on from early comments around UK banks one switch we are considering is outlined below:

1 Gain some UK Banking Exposure

As touched on earlier we believe the UK Banking sector is “looking for a low” which of course doesn’t mean its found one, especially considering the huge underperformance over recent years. This is a very contrarian call but that’s where the big bucks can be made when your right.

MM is looking for a bottom / catalyst for the UK Banking sector to rally.

Lloyds Banking Group (LLOY LN) Chart

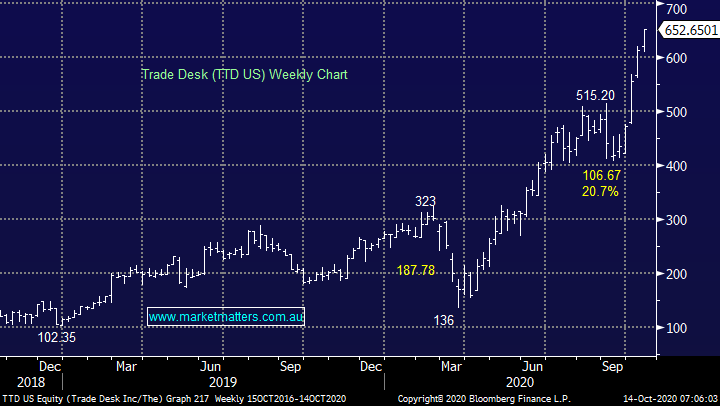

2 Trim / sell a tech outperformer

While we do believe that the global business make up has experienced a massive structural shift towards tech over the last decade all the best stocks can run too hard too fast e.g. in 2020 alone Apple Inc (AAPL US) has corrected 25% and 35% respectively. Our position in Trade Desk (TTD US) instantly comes to mind, its already up over 150% in just 6-months.

MM is looking blow-off moves in our tech holdings to take some profit.

Trade Desk (TTD US) Chart

MM Global Macro ETF Portfolio

Again no change to our positions, MM’s Global Macro Portfolios cash position remains at 4% : https://www.marketmatters.com.au/new-global-portfolio/

Similarly, to our International Portfolio we are happy with our current portfolio mix believing it’s time to sit back and carefully monitor our holdings.

One position that is on close watch is our Emerging markets position via the iShares ETF (IEM) which has rallied to fresh post March highs and by definition is at risk of failure however the influential Chinese market remains bullish with an initial target ~8% higher hence we are far from panicking at this stage.

Emerging Markets iShares ETF (IEM) Chart

Chinas Shenzhen CSI 300 Index Chart

Have a great day!

The Market Matters Team

Disclosure

Market Matters may hold stocks mentioned in this report. Subscribers can view a full list of holdings on the website by clicking here. Positions are updated each Friday, or after the session when positions are traded.

Disclaimer

All figures contained from sources believed to be accurate. All prices stated are based on the last close price at the time of writing unless otherwise noted. Market Matters does not make any representation of warranty as to the accuracy of the figures or prices and disclaims any liability resulting from any inaccuracy.

Reports and other documents published on this website and email (‘Reports’) are authored by Market Matters and the reports represent the views of Market Matters. The Market Matters Report is based on technical analysis of companies, commodities and the market in general. Technical analysis focuses on interpreting charts and other data to determine what the market sentiment about a particular financial product is, or will be. Unlike fundamental analysis, it does not involve a detailed review of the company’s financial position.

The Reports contain general, as opposed to personal, advice. That means they are prepared for multiple distributions without consideration of your investment objectives, financial situation and needs (‘Personal Circumstances’). Accordingly, any advice given is not a recommendation that a particular course of action is suitable for you and the advice is therefore not to be acted on as investment advice. You must assess whether or not any advice is appropriate for your Personal Circumstances before making any investment decisions. You can either make this assessment yourself, or if you require a personal recommendation, you can seek the assistance of a financial advisor. Market Matters or its author(s) accepts no responsibility for any losses or damages resulting from decisions made from or because of information within this publication. Investing and trading in financial products are always risky, so you should do your own research before buying or selling a financial product.

The Reports are published by Market Matters in good faith based on the facts known to it at the time of their preparation and do not purport to contain all relevant information with respect to the financial products to which they relate. Although the Reports are based on information obtained from sources believed to be reliable, Market Matters does not make any representation or warranty that they are accurate, complete or up to date and Market Matters accepts no obligation to correct or update the information or opinions in the Reports. Market Matters may publish content sourced from external content providers.

If you rely on a Report, you do so at your own risk. Past performance is not an indication of future performance. Any projections are estimates only and may not be realised in the future. Except to the extent that liability under any law cannot be excluded, Market Matters disclaims liability for all loss or damage arising as a result of any opinion, advice, recommendation, representation or information expressly or impliedly published in or in relation to this report notwithstanding any error or omission including negligence.