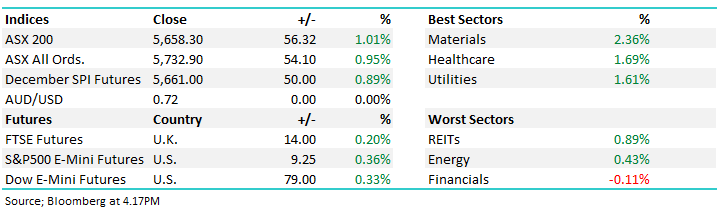

ASX bucks overseas weakness adding 1% (BHP)

WHAT MATTERED TODAY

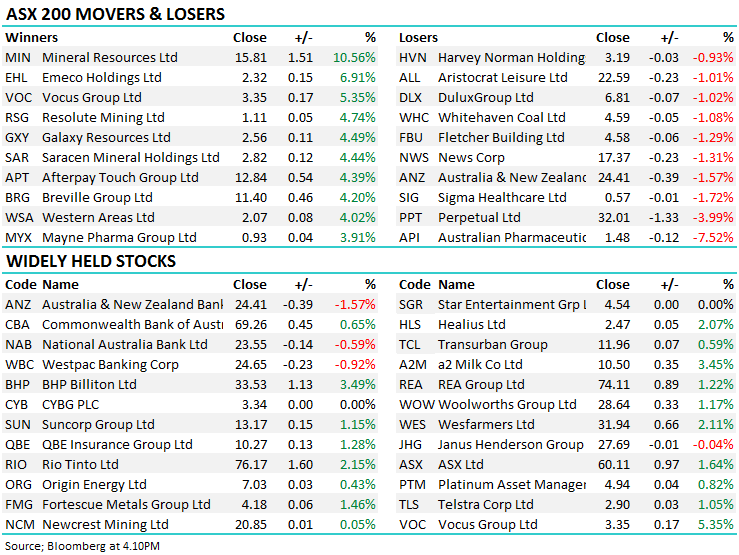

With the US market down ~500pts on Friday night our market was set for a test early on today and once again we’ve seen strong buying from the ~5600 area on the ASX 200, today it was the resource stocks that did the heavy lifting while the banks were mixed, ANZ the worst of them thanks to news on Friday of increasing capital requirements in New Zealand - more on that below. BHP was the biggest contributor on the upside today after they announced the special dividend amount of $1.02 to be paid in January, while we also saw strong buying for TPG Telecom (ASX: TPM) following ACCC induced weakness last week, while both Vocus (ASX: VOC) & Telstra (ASX:TLS) also enjoyed a more positive mood in the sector today putting on 5.35% and 1.05% respectively.

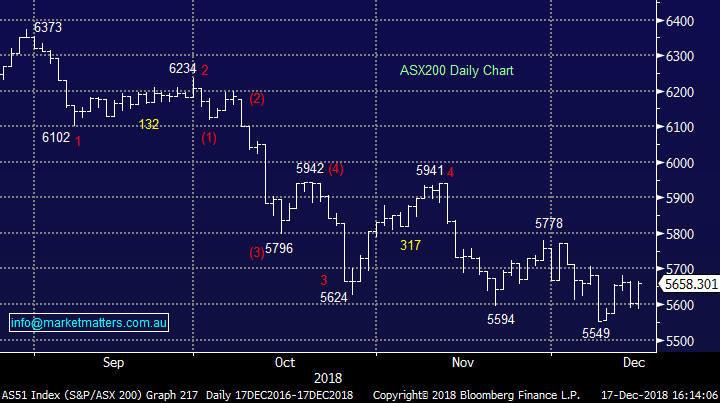

Technically, the market still looks positive for the Christmas rally to commence at a time when a lot seem to be losing conviction. As we wrote this morning, markets are all about probabilities rather than certainties. Simple statistics tell us that in the last 30 December’s, 25 of those have been positive while if we have a negative November, 27 out of the last 30 Decembers have been positive, implying a very good chance December should be positive. Experience tells me not to trade against such a strong seasonal trend, similar to our general caution towards the back end of May / April each year.

While local optimism in recent weeks has generally been dealt a blow from weakness overseas, it still seems like our market wants to move higher, we simply need some clear air internationally.

Overall today, the ASX 200 closed up +56 points or +1.00% to 5658. Dow Futures are currently trading up 87 points or +0.36%.

ASX 200 Chart

ASX 200 Chart

CATCHING OUR EYE;

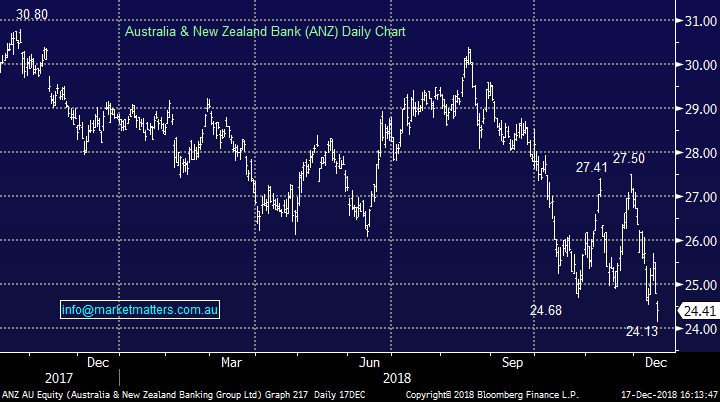

Broker Moves; Bells have cooled on ANZ in the last day or so as the New Zealand Central bank proposes to increase the amount of capital required for banks operating in the country. As a consequence Bells is suggesting that ANZ may need NZ$5b capital to adjust to the increased Tier 1 capital requirement to 16% from the prev. 8.5%; NAB may need NZ$3.4b, CBA NZ$2.9b and Westpac ~NZ$2b ANZ is the most exposed bank to the change given it has a higher proportion of earnings from NZ.

ANZ has been under pressure since the news broke on Friday afternoon – a little Christmas cheer from across the ditch for our already beaten up banking sector… We’ll look at the sector in more detail on Wednesday.

ANZ Bank (ASX:ANZ) Chart

ELSEWHERE:

· Panoramic Resources Rated New Outperform at Macquarie; PT A$0.70

· GWA Group Upgraded to Buy at Citi; PT A$3.69

· Inghams Downgraded to Sell at Citi; PT A$3.85

· ANZ Bank Downgraded to Hold at Bell Potter; PT A$26.80

· Vocus Upgraded to Hold at Morningstar

· Sonic Healthcare Downgraded to Hold at Morningstar

· Australian Pharma Downgraded to Hold at Morningstar

· oOh!media Upgraded to Buy at Morningstar

BHP Billiton (ASX:BHP) $33.53 / +3.49%: BHP went from strength to strength today, rallying throughout the session after completing the off market buyback on Friday. The buyback was well oversubscribed at the deepest discount of 14%, with shares to be bought back at $27.64/share after a 58% scale back is applied. Along with the buy-back announcement, BHP also announced a $US 1.02/share special dividend will be paid in January, however shares tendered will obviously not be eligible for the special dividend.

BHP (ASX:BHP) Chart

OUR CALLS

No changes today.

Have a great night

James, Harry & the Market Matters Team

Disclosure

Market Matters may hold stocks mentioned in this report. Subscribers can view a full list of holdings on the website by clicking here. Positions are updated each Friday, or after the session when positions are traded.

Disclaimer

All figures contained from sources believed to be accurate. Market Matters does not make any representation of warranty as to the accuracy of the figures and disclaims any liability resulting from any inaccuracy. Prices as at 13/12/2018

Reports and other documents published on this website and email (‘Reports’) are authored by Market Matters and the reports represent the views of Market Matters. The MarketMatters Report is based on technical analysis of companies, commodities and the market in general. Technical analysis focuses on interpreting charts and other data to determine what the market sentiment about a particular financial product is, or will be. Unlike fundamental analysis, it does not involve a detailed review of the company’s financial position.

The Reports contain general, as opposed to personal, advice. That means they are prepared for multiple distributions without consideration of your investment objectives, financial situation and needs (‘Personal Circumstances’). Accordingly, any advice given is not a recommendation that a particular course of action is suitable for you and the advice is therefore not to be acted on as investment advice. You must assess whether or not any advice is appropriate for your Personal Circumstances before making any investment decisions. You can either make this assessment yourself, or if you require a personal recommendation, you can seek the assistance of a financial advisor. Market Matters or its author(s) accepts no responsibility for any losses or damages resulting from decisions made from or because of information within this publication. Investing and trading in financial products are always risky, so you should do your own research before buying or selling a financial product.

The Reports are published by Market Matters in good faith based on the facts known to it at the time of their preparation and do not purport to contain all relevant information with respect to the financial products to which they relate. Although the Reports are based on information obtained from sources believed to be reliable, Market Matters does not make any representation or warranty that they are accurate, complete or up to date and Market Matters accepts no obligation to correct or update the information or opinions in the Reports. Market Matters may publish content sourced from external content providers.

If you rely on a Report, you do so at your own risk. Past performance is not an indication of future performance. Any projections are estimates only and may not be realised in the future. Except to the extent that liability under any law cannot be excluded, Market Matters disclaims liability for all loss or damage arising as a result of any opinion, advice, recommendation, representation or information expressly or impliedly published in or in relation to this report notwithstanding any error or omission including negligence.