Are Aussie banks cheap enough?

Banks are certainly on the nose and rightly so, some of the examples of poor behaviour coming from the Hayne Royal Commission were simply damming. When the Royal Commission was announced, a Senior Banking Analyst from the one of the well-known research houses suggested… "I don't consider the royal commission, or potential outcomes from the royal commission, will have any impact on the underlying fundamentals of the four major banks. And in particular, I don't see the wide economic moats being diminished in any shape or form. I see the banks' strong competitive advantages retained. I think it’s a good outcome for the major banks because most of the previous issues, allegations of misconduct have already been dealt with or are in the process of being dealt with. So, this announcement of royal commission is really more politics than good policy."

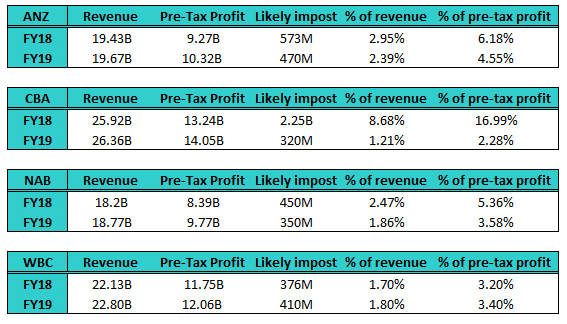

In fairness, they were not alone with this assessment however 10 months on and the environment for banks has clearly changed. In the past week we saw the last of the big 4 put numbers around the cost of ‘making good’ their bad behaviour, both in terms of prior costs and the forecasts for future expenditure. The below incorporates Bloomberg consensus data for earnings with the announcements from the banks themselves & data from Shaw’s Banking Analyst, Brett Le Mesurier.

These are projections for FY18 and FY19 for all bar CBA, which has already reported FY18 numbers (their FY18 number also includes AUSTRAC which was a CBA specific issue). The numbers above are now all known knowns, the market has digested them, and clearly they are bigger than anyone foreshadowed going into the Royal Commission. At a sector level its near on $5.2B over two years and if we throw in the amounts already spent to date + AMP, the number is around $7B, which is big.

The market will now price banks off FY19 earnings and we see an earnings hit of between 2.28% for CBA and 4.55% for ANZ – clearly from the above, CBA and WBC are positioned best moving forward. While these are significant numbers, now they’re out in the market it’s one less piece of ‘uncertainty’ for the banks. Arguably, this should now become less of an issue.

Weakness in housing…

One interesting correlation is between bank share prices versus housing data, specifically auction clearance rates. National house prices have now fallen 2.7% since peaking in September 2017, with Sydney being the hardest hit down by 6.1% versus Hobart which was up +9.3%. To put these into context, over the past 10 years, national house prices have risen by 44% with Sydney up by more than 100% over that time. House prices are a national past time in Australia and right now the media are doing their bit to stoke concerns.

These are projections for FY18 and FY19 for all bar CBA, which has already reported FY18 numbers (their FY18 number also includes AUSTRAC which was a CBA specific issue). The numbers above are now all known knowns, the market has digested them, and clearly they are bigger than anyone foreshadowed going into the Royal Commission. At a sector level its near on $5.2B over two years and if we throw in the amounts already spent to date + AMP, the number is around $7B, which is big.

The market will now price banks off FY19 earnings and we see an earnings hit of between 2.28% for CBA and 4.55% for ANZ – clearly from the above, CBA and WBC are positioned best moving forward. While these are significant numbers, now they’re out in the market it’s one less piece of ‘uncertainty’ for the banks. Arguably, this should now become less of an issue.

Weakness in housing…

One interesting correlation is between bank share prices versus housing data, specifically auction clearance rates. National house prices have now fallen 2.7% since peaking in September 2017, with Sydney being the hardest hit down by 6.1% versus Hobart which was up +9.3%. To put these into context, over the past 10 years, national house prices have risen by 44% with Sydney up by more than 100% over that time. House prices are a national past time in Australia and right now the media are doing their bit to stoke concerns.