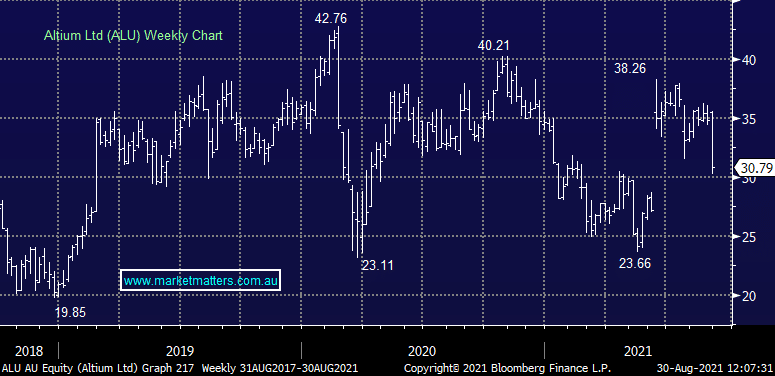

Altium (ALU) shares drop with targets pushed back

FY21 result: Shares getting hit today down 11% at time of writing after they beat consensus for FY21 and upgraded revenue guidance for FY22 however downgraded margin guidance, now expecting EBITDA margin between 34%-36% (vs prior target 36-39%), implying EBITDA for FY22 between $70-78. Consensus for revenue in FY22 was $202m and EBITDA $75.5m, so guidance is above in terms of both revenue and EBITDA. The reaction from the market today is negative, a few reasons we suspect. Downgraded margin guidance implies a softer underbelly, unaudited financials at FY results is strange and rhetoric in the announcement and on the call today seemed almost too positive for the results delivered. Our (Shaw) Analyst Jules Cooper had this to say… We maintain our Buy rating and $38.50 PT (under review), which is in-line with the original Autodesk offer, although was verbally increased to around $40 according to press articles. On our forecasts, ALU is currently trading on FY22 EV/Adj EBITDA multiple of 41.2x, which is below the average multiple it has traded at since Feb 2019, when ALU’s industry transformation goal begun to be widely communicated (~43x).