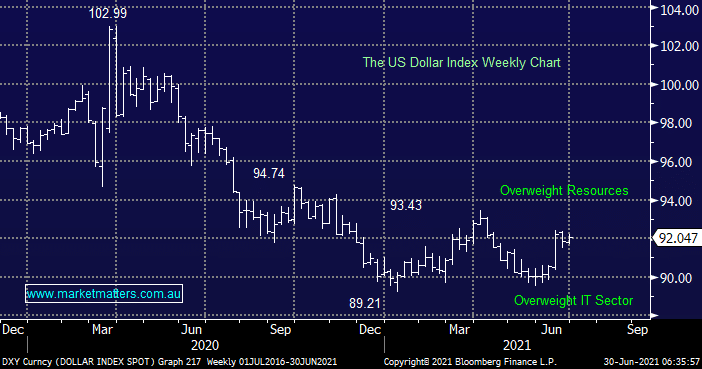

This month’s comments from the Fed sent the $US up in tandem with its shorter dated bond yields, after consolidating these gains for over a week, last night’s strong advance was triggered by global outbreaks of the COVID Delta strain which is questioning the speed of the future global economic recovery – unfortunately Australia was a contributing factor to this move. The strength in the greenback looks likely to amplify the recent outperformance from the tech sector over the resources / banks and moving forward MM continues to believe the sector rotation from value to tech has further to unfold but the next major point of inflection should be a high in the $US hence we are looking out for an optimum time to trim our tech exposure and potentially increase our holdings in the Resources Sector.

MM is looking for more upside from the $US

Add To Hit List