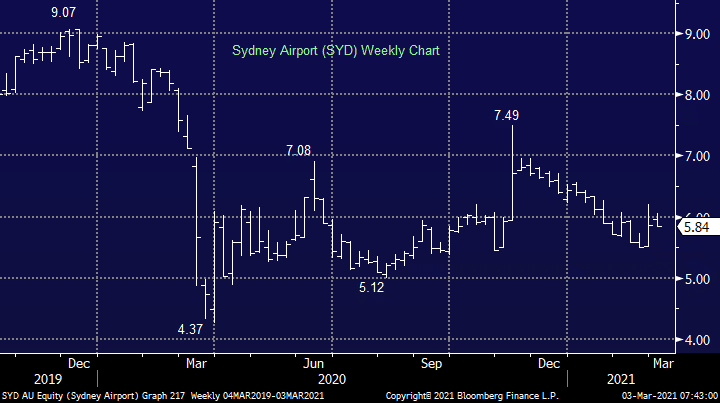

SYD should theoretically be a strong vaccine beneficiary as we all get the jab and start travelling again, however we don’t think that’s the case, not this year at least. SYD are expected to generate a small amount of free cash in 2021, but certainly not enough to pay a dividend, this will be reliant more on the time frame of international travel recommencing which is the real driver of an earnings recovery and thus resumption of dividends.

After SYD raised money in August, their net debt reduced down to $8.2bn however that is still a big number that has exposure to rising long dated interest rates. It’s also MM’s view that the recent pandemic and associated impact to (what were historically very stable earnings), will reduce the appetite of lenders to finance at such an aggressive rate. A greater risk premium on future refinancing, no dividends until 2022 in our view, and rising bond yields mean Sydney Airports is all too hard from an income perspective.

MM is cautious / bearish Sydney Airports (SYD)

Add To Hit List