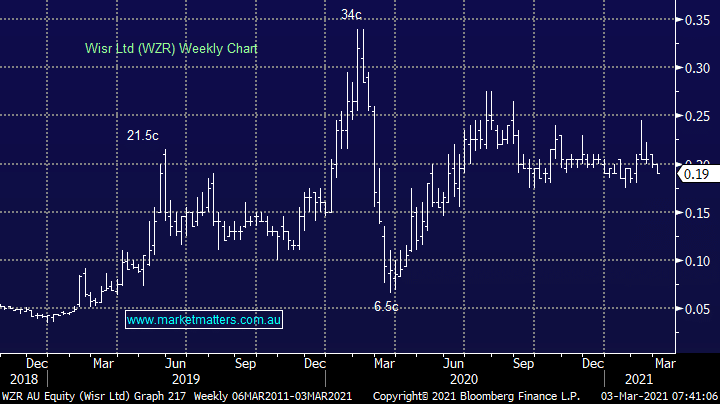

A small cap (~$200m) we have written about in the past, Wisr was added to the portfolio a few months after inception and has been weak even since. WZR is a finance business that they’ve packed up and called a ‘financial wellness eco-system’ which then feeds into a personal loan business. It recently topped $1b in originations and has moved into other verticals including car loans.

We like the business because it is gaining traction with the new products, it has a high average credit score for its customers (they only lend to very credit worthy people) and as it scales up, the funding costs fall and margins expand. The key here is that they’re solving a similar problem to the BNPL space, insofar as they’re targeting the exorbitant fee’s charged by credit card providers, and have built a nice piece of technology around this.

MM are bullish WZR – a key holding in the Emerging Companies Portfolio

Add To Hit List