Is QBE a takeover target?

What Mattered Today

A fairly soft session to kick off the trading week with the market opening lower following some slight weakness overseas + we also saw some Trumpism over the weekend which prompted selling in the $US on open this morning – seems that got investors into profit taking mode with some decent conviction, the index down more than ~60pts at the lows. Protectionism, anti-immigration, travel bans, walls and a number of other calls is starting to get investors somewhat nervous. We reiterate our view that selling strength on the expectation that we’ll get an opportunity to buy weakness courtesy of a handful of likely triggers is the way to play the market at the moment.

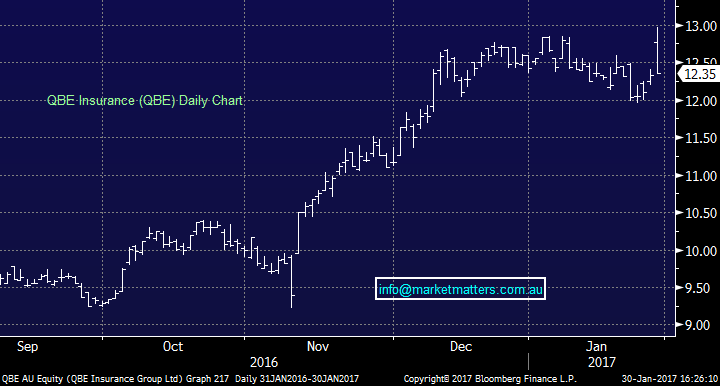

On a positive note, news that QBE might be in the sights of overseas acquirers got that stock up early on but the rally fizzled on the realisation that a takeover, at the prices discussed ($15) would not get shareholder support. More on that below.

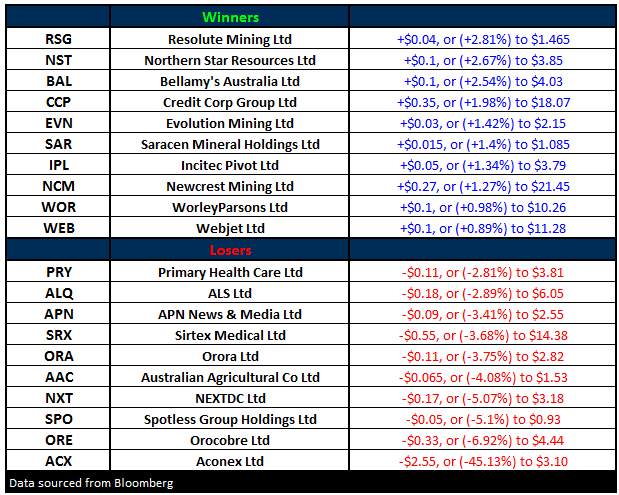

Elsewhere, another BIG downgrade from a high PE stock Aconex (ACX) - which finished down 45% on its lows, while Servcorp (SRV) also lowered guidance and was smacked by 19%. On the flipside, Warnambool Cheese (WCB) got a takeover bid from its major shareholder Saputo which saw that stock up almost 24% - although not sure who else owns the stock given liquidity is so low.

Golds did well with a number of production reports dropping today – Newcrest (NCM) of most interest to us with the stock moving higher by +1.27%

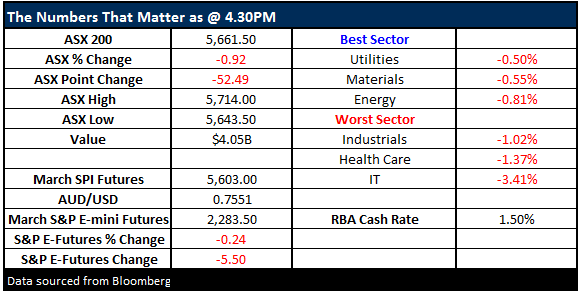

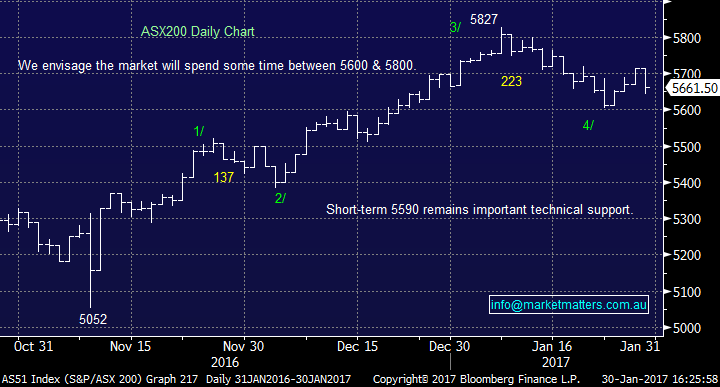

We had a range today of +/-65 points, a high of 5708 a low of 5643 and a close of 5661, off -52pts or -0.92%.

ASX 200 Intra-Day Chart

ASX 200 daily chart

QBE Insurance; There were a couple of articles out last week that were fairly vague around the potential for a QBE takeover however some meat on the bone in one out Friday and this got some airtime in the AFR this morning. According to media, Alliance is keen to BUY QBE for around $20bn or $15 a share and that got buyers revved up this morning with the stock hitting a high of $12.97 only to close at $12.35. We own QBE and from our own perspective, $15 (for a takeover) is too cheap. Insurance is at the bottom of the cycle and QBE’s earnings are extremely leveraged to higher US Bond yields. Every 1% increase in US bond yields adds $US250 million to the QBE bottom line. A 22% premium to the last traded price is simply too low. The art of investing is buying low, selling high. QBE (unfortunately) have been guilty of buying high, with a string of (now) overpriced acquisitions. Surely they would not then turnaround and SELL low?

Aconex (ACX); A very rough day for ACX with shares down more than 45% following downgraded guidance – the construction software coy which has been a mkt darling in recent times downgraded guidance by somewhere between 10% & 32% for 2016-17, and think now they’ll do earnings of $15-$18m versus $22-$25m expected. They used the old excuse of ‘Trump’ and ‘BREXIT’ for unsettling sales which is pretty hard to digest. Still on a high PE and now with weak earnings momentum. Give it a wide birth.

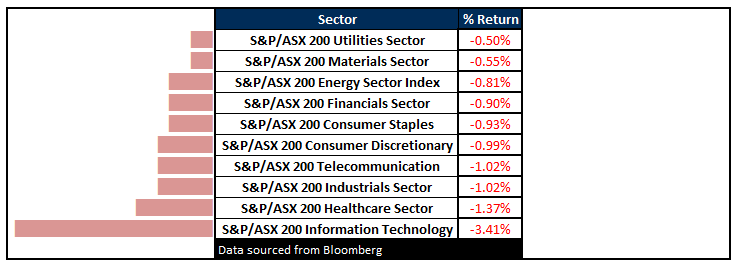

Sectors

ASX 200 Movers

Disclosure

Market Matters may hold stocks mentioned in this report. Subscribers can view a full list of holdings on the website by clicking here. Positions are updated each Friday.

Disclaimer

All figures contained from sources believed to be accurate. Market Matters does not make any representation of warranty as to the accuracy of the figures and disclaims any liability resulting from any inaccuracy. Prices as at 30/01/2017. 5.00PM.

Reports and other documents published on this website and email (‘Reports’) are authored by Market Matters and the reports represent the views of Market Matters. The MarketMatters Report is based on technical analysis of companies, commodities and the market in general. Technical analysis focuses on interpreting charts and other data to determine what the market sentiment about a particular financial product is, or will be. Unlike fundamental analysis, it does not involve a detailed review of the company’s financial position.

The Reports contain general, as opposed to personal, advice. That means they are prepared for multiple distributions without consideration of your investment objectives, financial situation and needs (‘Personal Circumstances’). Accordingly, any advice given is not a recommendation that a particular course of action is suitable for you and the advice is therefore not to be acted on as investment advice. You must assess whether or not any advice is appropriate for your Personal Circumstances before making any investment decisions. You can either make this assessment yourself, or if you require a personal recommendation, you can seek the assistance of a financial advisor. Market Matters or its author(s) accepts no responsibility for any losses or damages resulting from decisions made from or because of information within this publication. Investing and trading in financial products are always risky, so you should do your own research before buying or selling a financial product.

The Reports are published by Market Matters in good faith based on the facts known to it at the time of their preparation and do not purport to contain all relevant information with respect to the financial products to which they relate. Although the Reports are based on information obtained from sources believed to be reliable, Market Matters does not make any representation or warranty that they are accurate, complete or up to date and Market Matters accepts no obligation to correct or update the information or opinions in the Reports.

If you rely on a Report, you do so at your own risk. Any projections are estimates only and may not be realised in the future. Except to the extent that liability under any law cannot be excluded, Market Matters disclaims liability for all loss or damage arising as a result of any opinion, advice, recommendation, representation or information expressly or impliedly published in or in relation to this report notwithstanding any error or omission including negligence.

To unsubscribe. Click Here