Stocks marginally higher into the weekend

WHAT MATTERED TODAY

The market opened well this morning trading up more than +200pts at one stage as some pent up buying hit the screens, however the jitters crept in late in the day and the usual Friday afternoon sell-off took hold, stocks pulling back from early highs. US Futures traded in the opposite direction today, they were down early when we were up before edging higher throughout the day. A more subdued night in the US last night needs to be backed up by another drop in volatility tonight, high vol is unnerving.

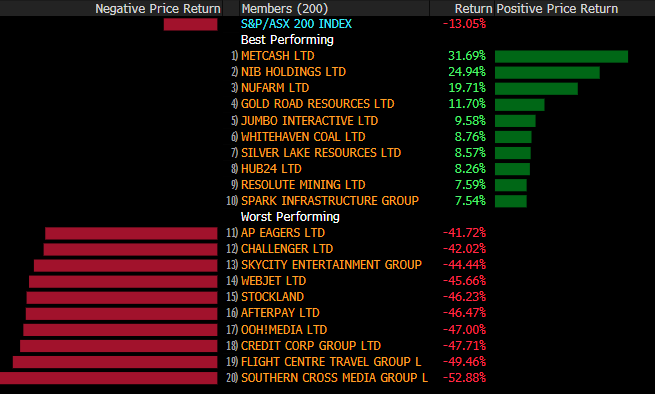

The tables below that look at stocks and sector move over the week is fairly astonishing, the index down 13% however the worst 10 performances in the ASX 200 were down more than 40% each in 5 trading sessions. On the market today, Real-Estate stocks bounced back after a horrible Thursday, +9% after falling -15% yesterday while the energy stocks enjoyed an uptick in the Oil price

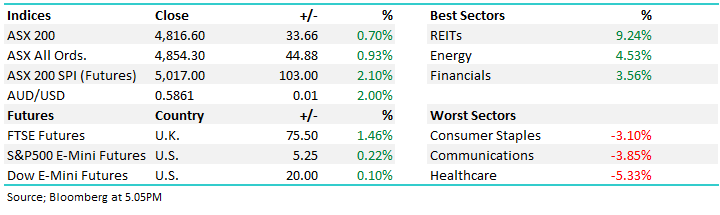

Overall, the ASX 200 added +33pts / +0.70% today to close at 4816 - Dow Futures are trading up +177pts/ 0.90%.

It’s been a huge week on the desk, totally exhausted and looking forward to the weekend. Stay safe all.

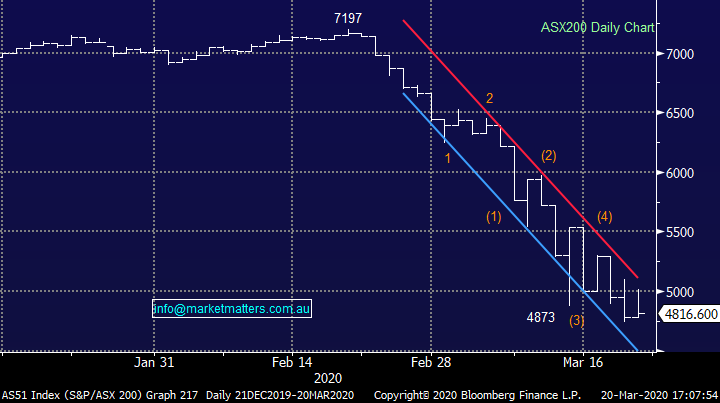

ASX 200 Chart

ASX 200 Chart

CATCHING MY EYE:

Sectors this week

Source: Bloomberg

Stocks this week

Source: Bloomberg

BROKER MOVES:

· Medibank Private Raised to Neutral at Macquarie; PT A$2.65

· Aurizon Raised to Outperform at Macquarie; PT A$5.52

· Harvey Norman Raised to Outperform at Macquarie; PT A$3.10

· Afterpay Raised to Neutral at UBS; PT A$13.20

· Transurban Raised to Outperform at Macquarie; PT A$14.47

· NAB Raised to Outperform at Macquarie; PT A$22

· Regis Resources Raised to Sector Perform at RBC

· Boral Raised to Buy at Citi; PT A$3

· Monadelphous Raised to Buy at Morningstar

· Domino's Pizza Enterprises Raised to Buy at Morningstar

· Bluescope Raised to Buy at Morningstar

· Cromwell Property Raised to Buy at Morningstar

· SCA Property Raised to Buy at Morningstar

· Sonic Healthcare Cut to Hold at Jefferies; PT A$23.40

· BHP Group PLC Raised to Buy at Deutsche Bank; PT 1,450 pence

· ANZ Bank Raised to Outperform at Credit Suisse; PT A$22.80

· NAB Raised to Outperform at Credit Suisse; PT A$19.50

· BHP ADRs Raised to Buy at Deutsche Bank

· Sandfire Resources Raised to Neutral at Goldman; PT A$4.10

· OZ Minerals Raised to Neutral at Goldman; PT A$7.90

· Alumina Raised to Buy at Goldman; PT A$1.90

· GUD Holdings Cut to Neutral at JPMorgan; PT A$1.28

· REA Group Raised to Buy at Jefferies; PT A$85.90

· Carsales.com Cut to Hold at Jefferies; PT A$13.04

· Medibank Private Raised to Outperform at Credit Suisse; PT A$3

· Gold Road Rated New Buy at Hartleys Ltd; PT A$1.55

OUR CALLS

No changes to the portoflios today

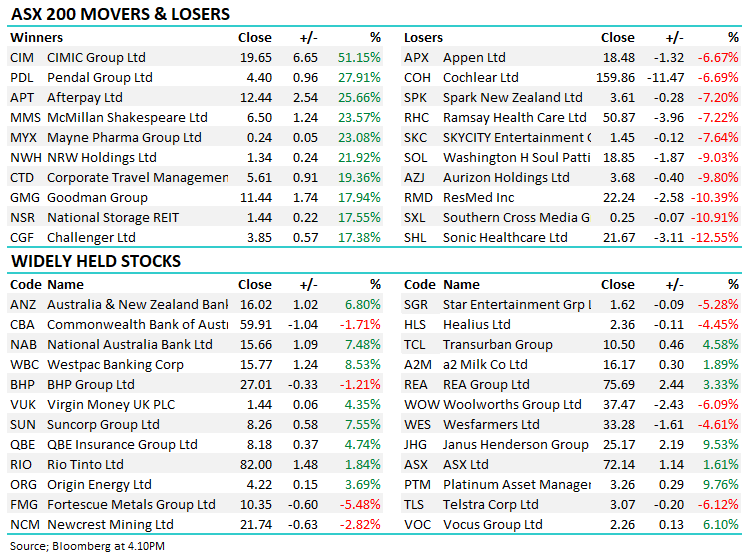

Major Movers Today

Have a great night

James, Harry & the Market Matters Team

Disclosure

Market Matters may hold stocks mentioned in this report. Subscribers can view a full list of holdings on the website by clicking here. Positions are updated each Friday, or after the session when positions are traded.

Disclaimer

All figures contained from sources believed to be accurate. All prices stated are based on the last close price at the time of writing unless otherwise noted. Market Matters does not make any representation of warranty as to the accuracy of the figures or prices and disclaims any liability resulting from any inaccuracy.

Reports and other documents published on this website and email (‘Reports’) are authored by Market Matters and the reports represent the views of Market Matters. The Market Matters Report is based on technical analysis of companies, commodities and the market in general. Technical analysis focuses on interpreting charts and other data to determine what the market sentiment about a particular financial product is, or will be. Unlike fundamental analysis, it does not involve a detailed review of the company’s financial position.

The Reports contain general, as opposed to personal, advice. That means they are prepared for multiple distributions without consideration of your investment objectives, financial situation and needs (‘Personal Circumstances’). Accordingly, any advice given is not a recommendation that a particular course of action is suitable for you and the advice is therefore not to be acted on as investment advice. You must assess whether or not any advice is appropriate for your Personal Circumstances before making any investment decisions. You can either make this assessment yourself, or if you require a personal recommendation, you can seek the assistance of a financial advisor. Market Matters or its author(s) accepts no responsibility for any losses or damages resulting from decisions made from or because of information within this publication. Investing and trading in financial products are always risky, so you should do your own research before buying or selling a financial product.

The Reports are published by Market Matters in good faith based on the facts known to it at the time of their preparation and do not purport to contain all relevant information with respect to the financial products to which they relate. Although the Reports are based on information obtained from sources believed to be reliable, Market Matters does not make any representation or warranty that they are accurate, complete or up to date and Market Matters accepts no obligation to correct or update the information or opinions in the Reports. Market Matters may publish content sourced from external content providers.

If you rely on a Report, you do so at your own risk. Past performance is not an indication of future performance. Any projections are estimates only and may not be realised in the future. Except to the extent that liability under any law cannot be excluded, Market Matters disclaims liability for all loss or damage arising as a result of any opinion, advice, recommendation, representation or information expressly or impliedly published in or in relation to this report notwithstanding any error or omission including negligence.