Property stocks lead the ASX higher (CAR)

WHAT MATTERED TODAY

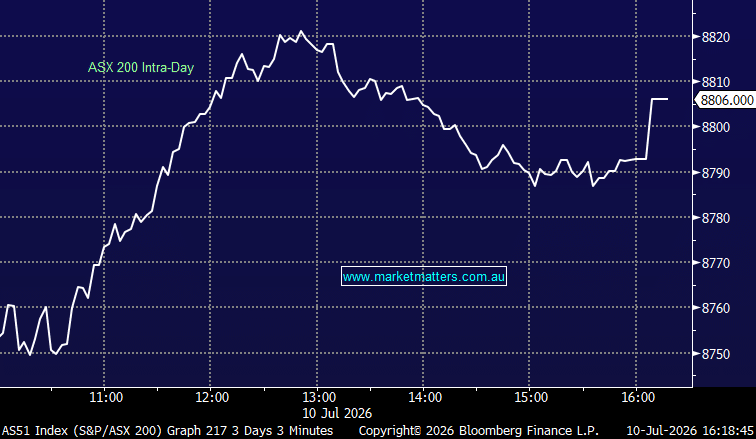

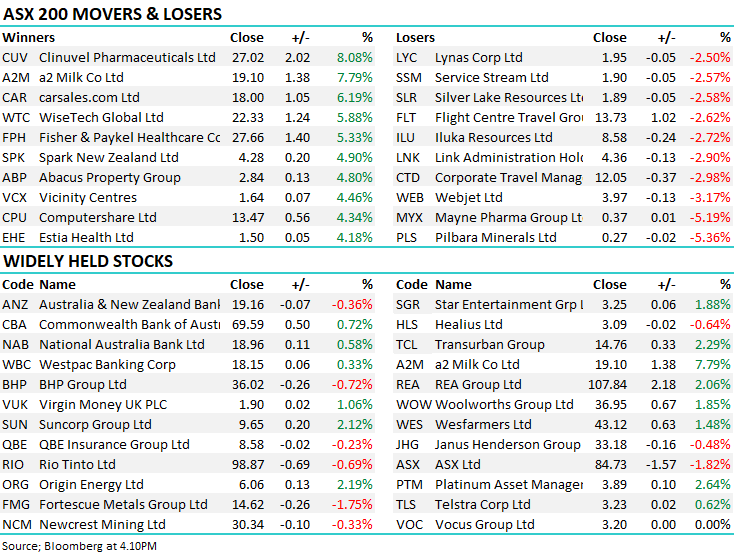

The market chopped around early on today, couldn’t really make up its mind until after lunch where stocks found their groove and the market rallied into the close, pushing sharply higher in the match. Real-Estate stocks were strong today, particularly the retail exposed names that benefitted from a very strong rebound in retail sales in the US overnight, this of course helped the actual retail stocks themselves. Carsales (CAR) out with a trading update today and the stock rallied +6%, Harry covers off on that one below, however the buying remained fairly broad based with 10 of 11 sectors up on the session the session. A quick note this afternoon with more detail tomorrow morning…

Overall, the ASX 200 added +50pts / 0.83% today to close at 5991 - Dow Futures are trading down -19pts/0.07%.

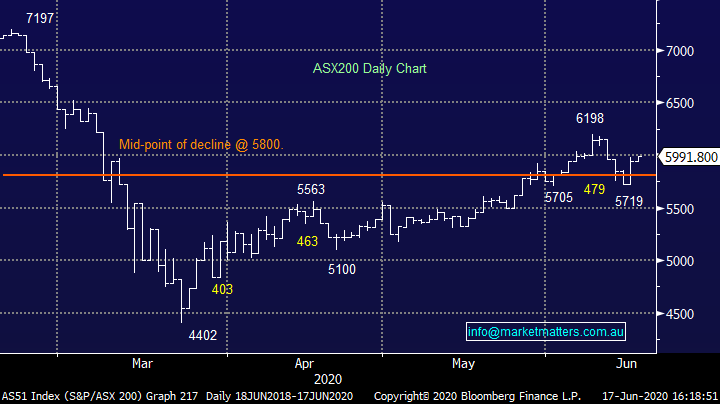

ASX 200 Chart

ASX 200 Chart

CATCHING MY EYE:

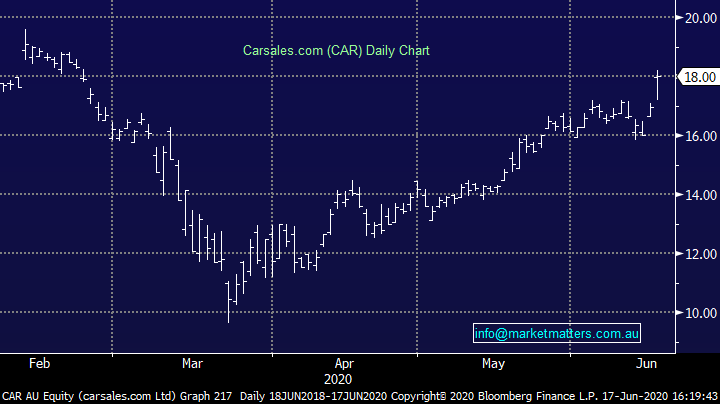

Carsales (CAR) +6.19%: one of the better performers today, the online vehicle classifieds saw shares jump on a reasonable guidance figure, talking up the rebound in activity since April. The company expects around 7.5% lower for the full year at $120-124m, on a fall of ~5.5% in revenue. The market was looking for $111m, guidance coming in at ~10% above expectations. As the economy beings to reopen, car buys have returned to the market, helping to reduce inventory on the site with some demand likely coming from people looking to avoid public transport amid the pandemic. On the international front, their South Korean market has rebounded similarly to the Australian market, but the Brazilian arm continues to lag with daily COVID cases still rising in the country.

Carsales were also able to renegotiate their debt facilities, with an additional $105m made available, with the bulk now expiring out in 2024. The flexibility this provides is key, with Carsales in good shape from a balance sheet perspective. Management are still keen to pay dividends at around 80% of net profit – on that basis shareholders could expect another 18c for the final div, taking it to 40c for the financial year.

Carsales (CAR) Chart

BROKER MOVES:

· Costa Raised to Neutral at Macquarie; PT A$2.87

· Alliance Aviation Cut to Market-Weight at Wilsons; PT A$3.14

· Westpac Raised to Equal-Weight at Morgan Stanley; PT A$18.10

· NAB Cut to Equal-Weight at Morgan Stanley; PT A$18.50

· Metcash Raised to Overweight at Morgan Stanley; PT A$3.30

· Viva Energy Raised to Overweight at JPMorgan; PT A$2

· ASX Cut to Underweight at Morgan Stanley; PT A$70

· Link Administration Cut to Underweight at Morgan Stanley

· Computershare Raised to Overweight at Morgan Stanley

· South32 Raised to Outperform at RBC; PT A$2.50

· Healius Cut to Hold at Morgans Financial Limited; PT A$2.96

· Iluka Cut to Neutral at JPMorgan; PT A$8.90

OUR CALLS

No changes today

Major Movers Today

Have a great night

James, Harry & the Market Matters Team

Disclosure

Market Matters may hold stocks mentioned in this report. Subscribers can view a full list of holdings on the website by clicking here. Positions are updated each Friday, or after the session when positions are traded.

Disclaimer

All figures contained from sources believed to be accurate. All prices stated are based on the last close price at the time of writing unless otherwise noted. Market Matters does not make any representation of warranty as to the accuracy of the figures or prices and disclaims any liability resulting from any inaccuracy.

Reports and other documents published on this website and email (‘Reports’) are authored by Market Matters and the reports represent the views of Market Matters. The Market Matters Report is based on technical analysis of companies, commodities and the market in general. Technical analysis focuses on interpreting charts and other data to determine what the market sentiment about a particular financial product is, or will be. Unlike fundamental analysis, it does not involve a detailed review of the company’s financial position.

The Reports contain general, as opposed to personal, advice. That means they are prepared for multiple distributions without consideration of your investment objectives, financial situation and needs (‘Personal Circumstances’). Accordingly, any advice given is not a recommendation that a particular course of action is suitable for you and the advice is therefore not to be acted on as investment advice. You must assess whether or not any advice is appropriate for your Personal Circumstances before making any investment decisions. You can either make this assessment yourself, or if you require a personal recommendation, you can seek the assistance of a financial advisor. Market Matters or its author(s) accepts no responsibility for any losses or damages resulting from decisions made from or because of information within this publication. Investing and trading in financial products are always risky, so you should do your own research before buying or selling a financial product.

The Reports are published by Market Matters in good faith based on the facts known to it at the time of their preparation and do not purport to contain all relevant information with respect to the financial products to which they relate. Although the Reports are based on information obtained from sources believed to be reliable, Market Matters does not make any representation or warranty that they are accurate, complete or up to date and Market Matters accepts no obligation to correct or update the information or opinions in the Reports. Market Matters may publish content sourced from external content providers.

If you rely on a Report, you do so at your own risk. Past performance is not an indication of future performance. Any projections are estimates only and may not be realised in the future. Except to the extent that liability under any law cannot be excluded, Market Matters disclaims liability for all loss or damage arising as a result of any opinion, advice, recommendation, representation or information expressly or impliedly published in or in relation to this report notwithstanding any error or omission including negligence.