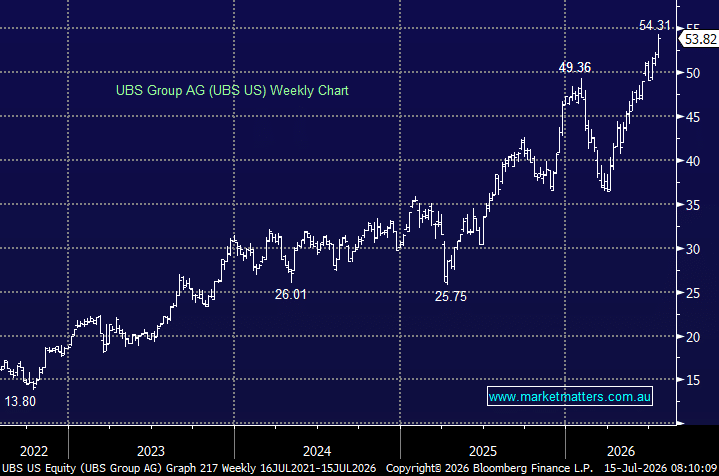

Like YETI covered above, UBS has now also reached our initial target and is trading toward the top of its recent range following a solid recovery in the share price. We continue to like the business and remain comfortable holding it in the International Equities Portfolio, although the near-term risk-reward is less compelling after the recent gains.

The valuation remains reasonable rather than outright cheap. UBS is trading on around 13.9x forward earnings, modestly above its five-year average of ~12.6x, but the multiple falls to roughly 12.8x FY27 earnings and 11.2x FY28 as profits continue to grow. Consensus expects adjusted EPS to rise from US$3.43 in FY26 to US$4.07 in FY27 and US$4.65 in FY28, underpinned by revenue growth, improving efficiency and further benefits from the Credit Suisse integration.

The earnings trajectory is the key attraction. Adjusted net income is forecast to increase from around US$11.2bn in FY26 to US$12.9bn in FY27 and US$14.1bn in FY28, while return on equity is expected to improve from ~12% to almost 14%. For context, CBA enjoys a sector leading ROE in Australia of 13.8%, and trades on a PE of 25x. UBS’s balance sheet is also strengthening, with net debt forecast to fall materially and book value continuing to rise.

Relative to global banking peers, UBS still trades at a premium, reflecting the strength of its wealth-management franchise and improving earnings quality. However, that premium has narrowed materially. The stock currently trades at around a 15% P/E premium to peers, compared with a five-year average premium of ~37%, suggesting the valuation is not excessive despite the recent share-price strength.

The major execution risk remains the integration of Credit Suisse, including cost reductions, capital management and the migration of clients and systems. The earnings forecasts also assume that management continues to deliver improving operating leverage, while global markets and wealth-management activity remain supportive.

We still regard UBS as a hold. The franchise is high quality, earnings momentum is strong and the valuation remains acceptable, but the stock has reached our initial target and is trading near the upper end of its recent range. As with YETI, we are increasingly conscious of locking in gains given the choppy nature of markets. We have UBS on a short leash ahead of their upcoming results on the 29th July.