Semiconductor stocks have remained in focus over the last 24-hours coming under heavy pressure on Monday, with the KOSPI falling almost 9%, despite the successful US listing of AI memory leader SK Hynix (SKHYV US) on Friday. Ironically, SK Hynix became the biggest drag on the index, plunging a record 15.4% in Seoul as investors rotated into its newly listed US ADRs, which surged +13% on debut.

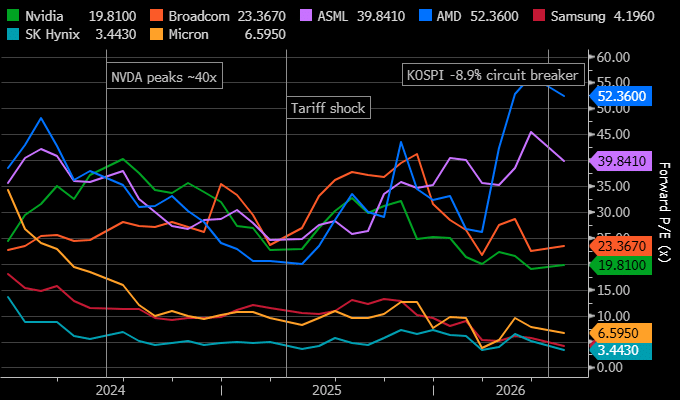

Panic selling of a crowded market is not a new song book for investors over recent years, but in this case it’s happening in an extremely profitable space, e.g. SK Hynix is expected to make a full-year 2026 profit of approximately US$15.6bn, more than News Corp’s (NWS) market cap! The sell-off has created a clear divide across the semiconductor sector. Memory names such as Micron, and by extension SK Hynix and Samsung, are now trading on near-trough valuations, while equipment and logic stocks remain relatively expensive despite the correction.

chart

Major semiconductor names valuations – Source Bloomberg

chart

Major semiconductor names valuations – Source Bloomberg

The key question is whether the memory cycle has peaked. Samsung’s “beat but sell” reaction and SK Hynix’s sharp decline suggest the market is increasingly pricing in that risk, rather than assuming AI-driven demand has permanently reshaped the industry’s traditional boom-and-bust cycle. Even TSMC’s record revenue failed to lift sentiment, highlighting that investors now want clear evidence that AI demand can continue to justify elevated earnings expectations.

The recent moves are reminiscent of a commodity cycle, where it is often better to buy producers on high valuation multiples than low ones. Low valuations typically coincide with elevated commodity prices and peak earnings, but those high prices also encourage new supply. That same dynamic is now emerging in semiconductors as manufacturers accelerate investment and expand capacity.

Conversely, high valuations often reflect depressed earnings and weak underlying prices, when supply growth is being curtailed and the foundations for the next recovery are forming. In cyclical industries, that can be the more attractive time to buy.

As the old saying goes, the cure for high prices is high prices, just as the cure for low prices is low prices. Prices ultimately drive the supply response that resets the cycle

At this stage, we don’t believe the cycle is over for Semi’s, but we do believe the market got “too long”, illustrated by the ~US$50bn that poured into leveraged positions at its peak across the space, and as we’ve witnessed this year, washouts of such crowded positioning can be deeper and more painful than many imagine.

-

The recent washout in semiconductor stocks does have hallmarks of capitulation, and our bias is that the worst of the selling may soon be behind us, but this is not a trend to fight for the faint hearted!

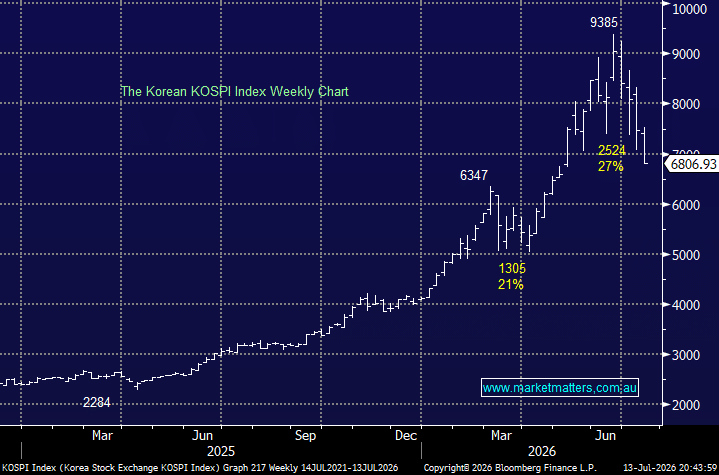

MM is very cautiously bullish towards the KOSPI below the psychological 7000 level

Add To Hit List