Hi Debbie,

For subscribers not familiar with Amotiv (AOV) it’s a ~$900mn automotive aftermarket group that designs, manufactures and distributes vehicle parts and accessories—including towing, 4WD, electrical and lighting products—across Australia, NZ and international markets through trade, retail and OEM channels.

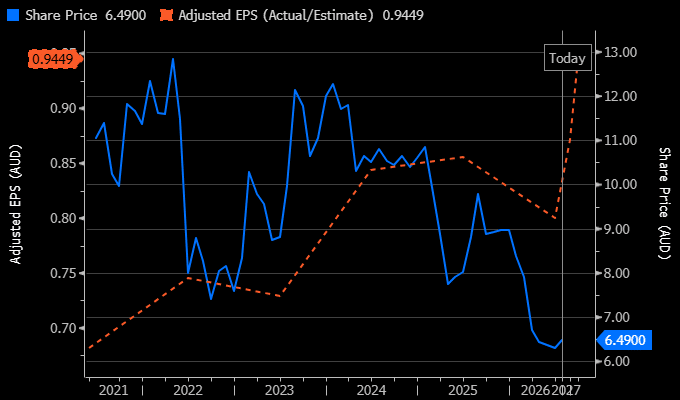

The chart below illustrates divergence between the flat earnings trend and the sharply declining share price caused by the significant multiple compression AOV has experienced since its 2024 highs – the mispricing you are alluding to.

However, AOV has underperformed dramatically since mid-2023, with a string of earnings misses, a major guidance downgrade, plus a large impairment driving the stock down sharply while the ASX200 gained over 30%. ARB, which operates in a similar space, has experienced a similar fate.

- FY24 miss (August 2024): Net profit of $98.8m fell short of the $101.1m consensus, while revenue of $987.2m also missed expectations.

- 1H25 disappointment (February 2025): Net profit of $33m was 37% below consensus, weighed down by New Zealand impairments and restructuring costs.

- FY25 downgrade (April 2025): AOV cut guidance to only marginal revenue growth and lower underlying EBITA, citing prolonged reseller destocking.

- FY25 result (August 2025): The company reported a $106.3m statutory loss, largely due to an APG impairment, while underlying EBITA fell 1.3% to $192m and missed forecasts. FY26 guidance of around $195m implied only modest growth.

AOV’s ~47% price decline since August 2023 has been driven primarily by P/E multiple compression (down ~34%), with forward EPS estimates broadly flat (down only around 5%). The stock has simply de-rated from ~14x to ~8.5x forward earnings as confidence in earnings delivery has eroded.

Following the above series of misses & downgrades it’s not surprising the stock is “cheap” and if they can just meet expectations through 2026/7 the stocks likely to perform well, supported by it ~6.3% forecast yield (Bloomberg consensus). In terms of adding it to the Income Portfolio, it’s a bit spicy for that lower risk portfolio.