Yesterday, platform provider Netwealth (ASX: NWL) rallied +6.73% to $24.43 after securing a platform mandate from Morgan Stanley Wealth Management Australia and guiding to FY27 net inflows of $18-20bn. While management flagged higher technology investment would compress earnings margins next year, the market focused on the strong growth outlook, with the company targeting an EBITDA margin of 47% and ambitions to double FUA to over A$250 billion within four years.

- The ASX platform providers have struggled in 2026: HUB24 (-13%), Praemium (-12%), Netwealth (-5%), while Insignia Financial is the only name in positive territory (+5%) following a takeover bid by US private equity firm CC Capital Partners.

The three main providers have been sold off on a combination of factors, some of which were more specific on the individual company fronts:

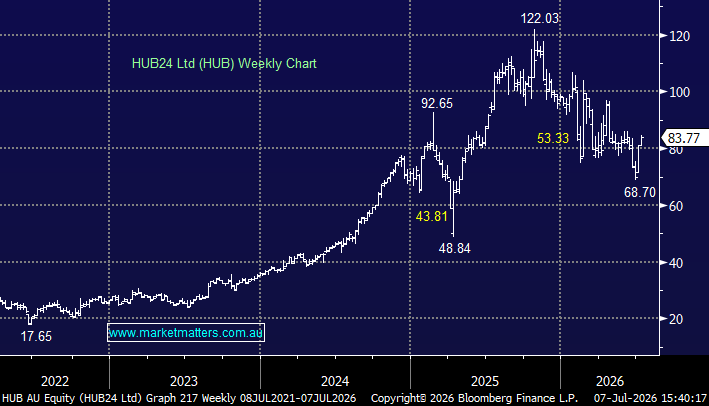

Valuation Contraction: Having enjoyed years of multiple expansion, HUB24 and Netwealth entered FY26 priced for near perfection. However, HUB24’s 3Q platform inflows of $3.98bn were down 19% year-on-year, while war-driven market volatility and signs of moderating market share gains suggested growth may be normalising.

Cost Pressures & Margin Compression: Netwealth’s 1H26 result illustrated the impact of rising investment costs, with the company reporting a $2.2m net loss and lowering FY26 EBITDA margin guidance to around 49%. While margins were expected to improve in the 2H, the downgrade weighed heavily on investor sentiment and the share price.

AI Disruption Fears: AI has weighed on sector valuations, although wealth platforms are widely viewed as less exposed than traditional software businesses. We believe AI is more likely to enhance adviser productivity and support platform inflows than disrupt the business model, though concerns around long-term valuation multiples have persisted.

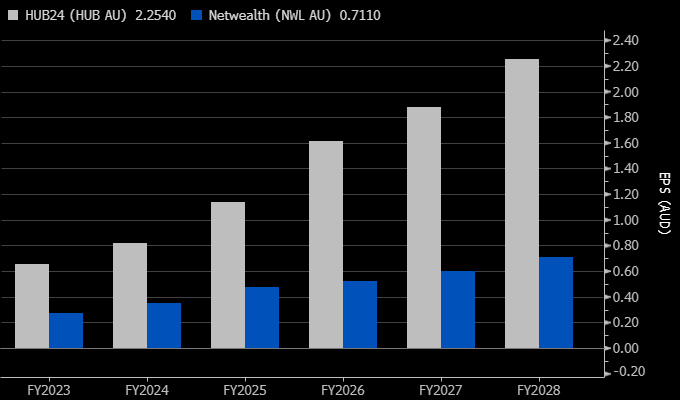

HUB is forecast to grow its earnings per share (EPS) by ~60% between FY25 to FY27, while NWL growth is on track for a relatively muted ~26%. Both growth numbers are impressive, but we prefer to stick with the strength at this stage:

- HUB has been MM’s preferred platform provider over the years, and that remains the case, although both NWL and HUB look interesting at current levels.

chart

Consensus EPS Growth for NWL and HUB – Source Bloomberg

chart

Consensus EPS Growth for NWL and HUB – Source Bloomberg

We sold HUB back in February on AI Disruption concerns which have been a contributing factor to valuation pressure, leading to a broader de-rating of high-multiple growth stocks. However, after correcting well over 40%, we believe value has returned to the stock and space. Three catalysts are combining to make us bullish on HUB today:

- We are bullish towards equities through 2026, which should benefit the platform providers.

- We believe calm is returning around AI and investors are recognising that the likes of HUB and NWL can actually be beneficiaries.

- The recent budget has elevated stocks over property, as an asset class in Australia, another tailwind for HUB and NWL.

*Watch for alerts: HUB is on our radar as we look to switch out of QBE, which has delivered our targeted gains.

- We like the risk/reward towards HUB below $85 with an initial target above $100, or up +20%.

MM is bullish towards HUB below $85

Add To Hit List