In an update last week, HMC announced another important step in broadening its funds management platform, securing commitments from two global institutional investors to deploy up to $1.35 billion into private credit.

This is strategically significant. HMC’s private credit business has so far been built largely through wholesale and high-net-worth investors, with more than $2 billion of assets under management. Institutional backing expands the opportunity and gives HMC the chance to replicate some of the success it has already achieved in real estate.

Private credit is also an attractive business, supported by management fees and borrower-paid origination fees. The earnings benefit will build progressively, however, as part of the mandate is seeded from existing HMC funds and the remaining capital is deployed over time.

The main issue is the earnings reset into FY27. HMC is moving to a cleaner definition of operating earnings that excludes mark-to-market gains and losses on principal investments. This improves transparency, but also highlights the extent to which FY26 benefited from valuation gains and other non-recurring income.

HMC has guided to pre-tax operating earnings per share (EPS) of 40c for FY26 and outlined a pathway to maintain that level beyond FY27. Most brokers are more cautious, with UBS for instance forecasting 32.8c in FY27, reflecting the loss of revaluation gains, the wind-down of HMC Capital Partners and lower Energy Transition income. Cost savings, new private credit fees and the resumption of HealthCo distributions should provide some offset, making consensus too bearish in our view.

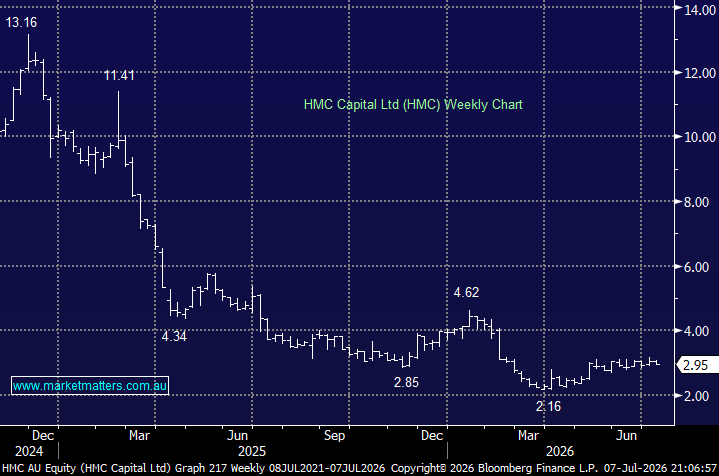

Despite the softer near-term earnings outlook, the valuation remains interesting. At ~$3, HMC trades on roughly 13x FY27 earnings, with a dividend yield of 4.1% (part franked). On UBS estimates, the market is valuing the underlying funds management platform at only around 3x FY27 EBITDA after allowing for its balance-sheet investments.

The discount does reflect legitimate concerns around earnings complexity, listed co-investments and the timing of new fund inflows. However, HMC’s fee-paying assets have grown rapidly, and the institutional private credit mandate adds another credible growth leg alongside real estate, digital infrastructure and energy transition.

- It must be noted, that HMC remains a higher-risk and more complex fund manager, with FY27 likely to mark a meaningful earnings reset. However, the private credit mandate is a strong endorsement of the platform and should improve the mix toward recurring fee income.

There is also the Healthscope issue that could be resolved. In early 2025, Healthscope had begun falling behind on rent owed to landlords, including HMC-managed HealthCo Healthcare & Wellness REIT (HCW) and the and the Unlisted Healthcare Fund (UHF). Its lenders ultimately appointed McGrathNicol as receiver in May 2025, while providing additional funding to keep the hospitals operating during a sale and restructuring process. Uncertainty over rental collections caused HCW to withdraw earnings guidance and suspend distributions to preserve liquidity. That reduced the distributions HMC received on its HCW investment and weighed on the value of HMC’s stake.

Healthscope did not threaten HMC Capital in the same way it threatened Healthscope’s lenders. HMC did not own the heavily indebted hospital operator; its managed funds owned the hospital real estate. However, the collapse exposed weaknesses in the original tenant underwriting and created a material problem for HCW and UHF. It reduced distributions, hit asset values, delayed fees and damaged confidence in HMC’s capital-allocation model.

HMC agreed to support HCW, including through management-fee deferrals. That meant some fee revenue and cash flow were delayed while the Healthscope situation is being worked through. The remaining task is to install financially sustainable operators and agree rents they can afford. That could involve different operators taking individual hospitals rather than one group replacing Healthscope across the entire portfolio. However, new leases may be struck on less favourable terms than the original Healthscope arrangements, which will most likely mean lower rents, landlord-funded capital expenditure, rent-free periods or incentives, lease restructuring and asset-value write-downs, if sustainable rent is below previous assumptions.

The positive is that the hospitals remain operational and the Healthscope rent position stabilised during the receivership. A successful transition to stronger operators would restore HCW distributions and remove a major overhang from HMC.

- Trading on ~13x FY27 earnings, the stock looks inexpensive, although further mandate wins and delivery against its cost and earnings targets will be important, as will a sustainable resolution around Healthscope, before the market gives HMC a higher multiple.

MM remains optimistic on HMC, looking for a turnaround in FY27

Add To Hit List