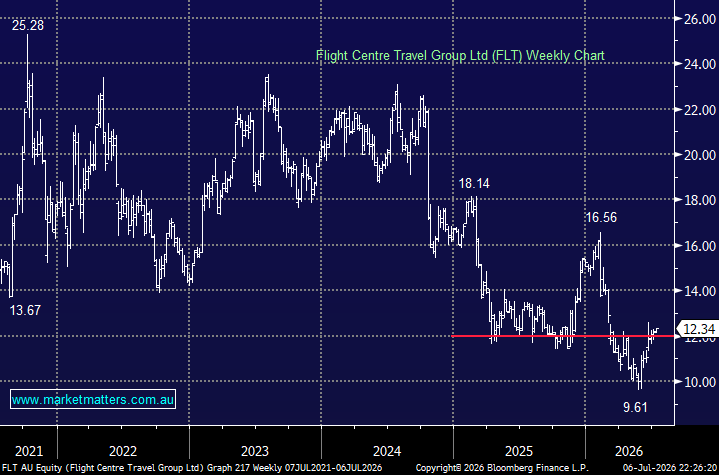

Flight Centre is one business that MM has successfully avoided over recent years, but it is starting to look interesting. We looked at it here last month after the company downgraded FY26 earnings guidance due to the Iran War, while at the same time announcing a supportive $200mn buyback – the downgrade, which was no major surprise, is feeling like a “washout low.” The stock is trading on the cheap side while paying a ~3.5% fully franked yield, but we acknowledge this is a mixture of a recovery and broadening story.

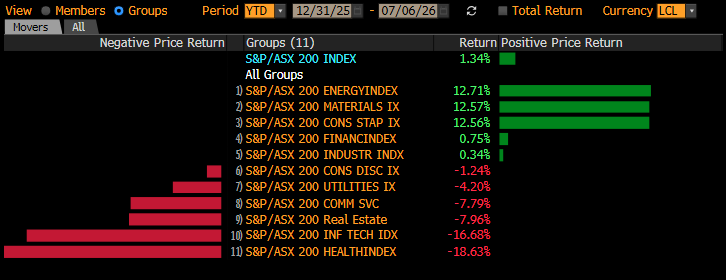

The company is undoubtedly well positioned if the RBA adopts a more dovish stance later in 2026, as we believe they will. When consumer confidence does improve, FLT is likely to benefit, and we’re already seeing the market pick a turn here with the consumer discretionary sector bouncing almost +12% in the last months as part of the broadening market recovery.

Importantly for us, the US remains Flight Centre’s largest long-term growth opportunity. Both FCM and Corporate Traveller have relatively low market share in a global corporate travel market where the company estimates its overall share is just 5%, leaving a substantial runway for expansion. Recently, US momentum has been strong, with Corporate Traveller USA posting +19% TTV growth in January 2026, and the broader Americas corporate business delivering +18% profit growth in the first half.

- At this stage, we see good risk/reward towards FLT with a recovery back towards $16 a strong possibility in our view.

MM is bullish towards FLT around $12

Add To Hit List