Hi Alain,

A great and well-timed question.

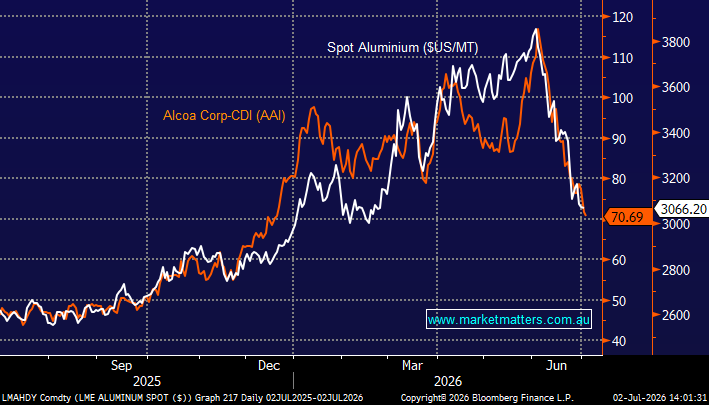

By Thursday Afternoon Alcoa (AAI) was trading down ~10% since it announced the acquisition of South32’s aluminium assets for up to US$5.6bn – a common move for purchasers in a M&A transaction. More importantly, AAI has now retreated ~40% from its May high, in line with the aluminium price.

Aluminium itself has given back much of its conflict-driven rally as three key headwinds emerged:

- First, the US-Iran ceasefire eased fears of supply disruptions through the Strait of Hormuz, unwinding the geopolitical risk premium that had built up during the conflict.

- Second, Chinese smelters ramped up production and exports to capitalise on elevated prices, helping alleviate global supply tightness.

- Finally, a run of weaker-than-expected Chinese economic data weighed on demand expectations, reinforcing the sell-off.

The combination proved painful, with aluminium recording its worst monthly decline since 2008 in June, falling ~20%, wiping out the gains made over the previous three months. We now feel the weakness in both AAI and Aluminium finally affords some decent risk reward with the metal still expected to play a critical role in the energy transition due to its light weight, strength and recyclability.

- Aluminium demand is set to be driven by electric vehicles, renewable energy infrastructure, electricity transmission and distribution, battery storage, and lightweight construction, with global electricity grid expansion emerging as one of the largest long-term growth drivers.

However, as you say electricity is the single largest input cost in aluminium production, accounting for around one-third of total smelting costs. While higher power prices can squeeze Alcoa’s margins, they also force higher-cost producers out of the market, tightening supply and supporting aluminium prices over the medium term, a dynamic that generally favours low-cost producers like Alcoa.

- Aluminium production being a high energy process is one of the reasons we prefer Copper over the coming years, but we do see them both trading higher.