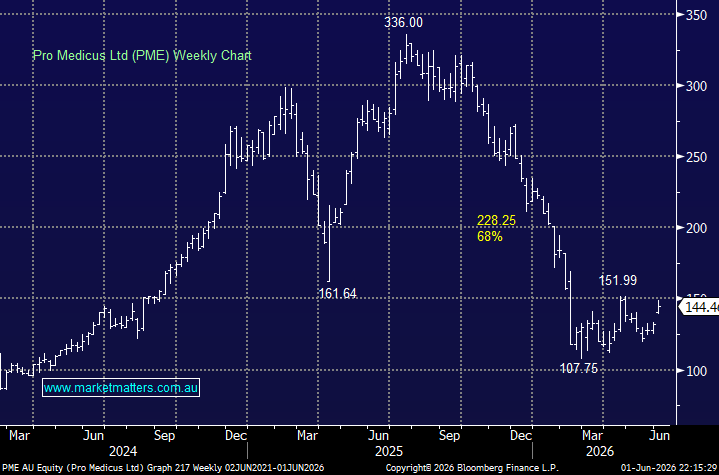

Pro Medicus (PME) was one of the market’s favourite stocks in 2025, and while its ~$15bn valuation against revenue of only around ~$260m triggered a valuation reset, the business itself has continued to execute exceptionally well. Importantly, the recent pullback has been driven far more by multiple compression than any deterioration in the company’s fundamentals. In our view, PME remains the highest-quality and arguably most defensively positioned software business on the ASX.

Its Visage 7 medical imaging platform is deeply embedded in the workflows of leading US hospital networks, where speed, reliability and clinical accuracy are mission-critical. This is not discretionary software that can be easily switched off or replaced. PME continues to maintain an exceptional customer retention record, while also winning major contracts against much larger competitors — a strong endorsement of the quality of its technology and the value it delivers to customers.

While AI disruption is a legitimate concern across software, we think Pro Medicus is one of the few names where AI is more likely to enhance the moat than erode it. Rather than replacing Visage, AI can make the platform more valuable by improving radiology workflows, accelerating image analysis, supporting detection tools and automating parts of the reporting process. Management has been actively embedding AI capabilities into Visage, including advanced breast cancer screening applications and its RadPath Hub, which integrates radiology and pathology data to support more sophisticated clinical decision-making.

The bear case remains valuation and execution rather than technology disruption. PME still trades on a premium multiple, leaving less room for disappointment, while US hospital budget cycles and the timing of large contract wins can create volatility. However, with only a modest share of the US imaging market, a mission-critical product, a long runway for new contract wins and clear leverage to AI-enabled healthcare digitisation, we think Pro Medicus remains one of the best-positioned structural growth stories on the ASX.

In a market beginning to rotate back toward quality software, PME looks exceptionally well placed. Investors often pay up for genuine scarcity, and PME offers exactly that: world-class technology, recurring revenue, strong margins, global growth potential and a product that is becoming more important, not less, as healthcare systems digitise.

We like PME as a business and see it as one of the highest-quality ways to gain exposure to software, AI and healthcare digitisation on the ASX. With the software sector turning higher, PME looks well placed for a recovery as investors scramble to regain exposure to genuine quality growth — watch for alerts.

MM is bullish towards PME around $145

Add To Hit List