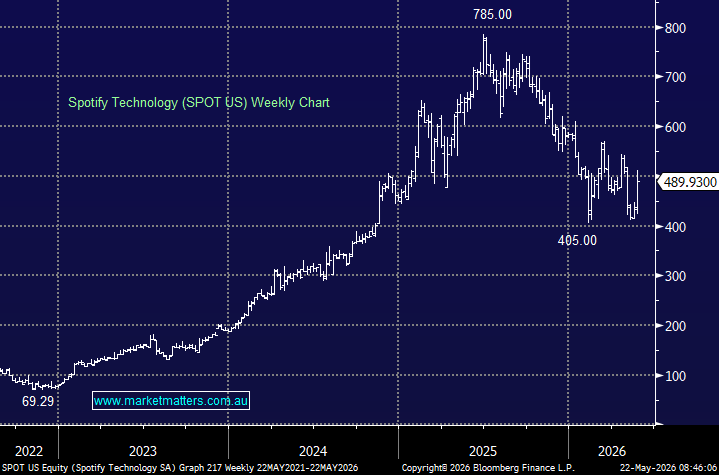

A very interesting investor day held by Spotify overnight, laying out a series of ambitious long-term targets and a broader premium product roadmap. The most obvious aspect we took from this update was that Spotify wants the market to think less about quarterly subscriber volatility and more about its ability to grow revenue, expand margins and monetise its very large user base more effectively over time. This is a big shift away from a land grab type approach to one focussed on sensible monetisation of their huge 300m user base.

The key details:

- Spotify is targeting mid-teens compound annual revenue growth through 2030.

- Management expects gross margins of 35-40% over that period.

- Operating margins are expected to be above 20% through 2030.

- The company continues to hold broader long-term ambitions of 1bn subscribers, €100bn in revenue, and gross margins above 40%.

- For the current quarter, Spotify expects operating income of €630m – which was ahead of ~ €580m consensus

- It expects to add 6m premium subscribers, taking the total to 299m.

- Spotify also announced a deal with Universal Music Group to launch an AI tool allowing users to create covers and remixes of songs.

- The AI product will be offered as a paid add-on for premium subscribers.

- A new feature called Reserved will identify top fans of selected artists and hold two live concert tickets for those users.

The market liked the combination of long-term financial ambition and new monetisation levers. Spotify has spent years building scale, but the bear case has often centred on whether it could ever generate meaningful margins given the economics of music royalties. The Investor Day went some way to addressing that, with management pointing to higher gross margins, operating leverage and new paid features as the next phase of the story.

The AI partnership with Universal is interesting because it gives Spotify a way to lean into AI without simply becoming a battleground with the music labels. By launching tools that are licensed and paid for, Spotify is trying to turn AI from a disruption risk into a revenue opportunity. If successful, it could increase engagement, add another subscription layer, and provide a new way to monetise super fans.

The Reserved ticketing feature also fits into this broader strategy. Spotify already has enormous data on listening behaviour, artist loyalty and fan engagement. Using that data to connect top fans with live music tickets is a logical extension of the platform and potentially opens the door to broader commerce opportunities over time.

The caveat is valuation and execution. Even after the rally, Spotify remains down around 15% in 2026 and around 36% over the past year. We bought SPOT in December of 2025, and we’re currently down ~19% on our position, with market concerns around subscriber momentum, costs and the durability of margin expansion the key factors, though we still believe these concerns are over blown, and the overnight update should certainly help to address these concerns.

- We remain positive on Spotify with higher conviction post the investor day.