H Paul,

Thanks for the kind words, it means a lot to the whole MM Team!

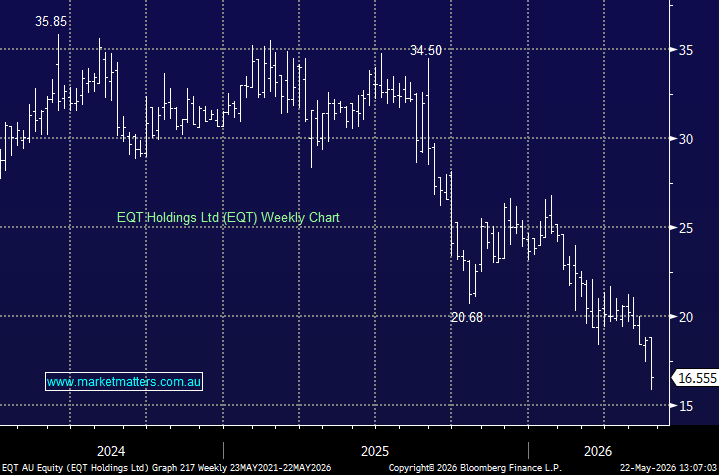

For subscribers not familiar with EQT, it’s a $440mn Melbourne based company which generates recurring fee income from trustee and fiduciary services, including acting as trustee for super funds, managed funds, estates and corporate structures. The business also earns revenue from wealth management and administration services, giving it a theoretically defensive earnings moat underpinned by regulation and long-term client relationships.

The stock has now more than halved despite steady revenue growth and an attractive fully franked yield, primarily due to its involvement in the collapse of the Shield and First Guardian Master Funds.

- This week ASIC has sued EQT’s superannuation subsidiary, over alleged failures relating to the First Guardian Master Fund that cost members an estimated $65–70 million.

This fiasco will have a lasting impact on it’s main intangible asset – trust. People pay EQT money because they trust them, which has been earnt over a long period of time. Their involvement in First Guardian has materially eroded this, and rightly so. It’s very hard to quantify what this will mean in the longer term, and we can fully understand why investors are exiting. The uncertainty around potential liabilities and lasting reputational damage is real.

- For this reason, EQT is in the too hard basket for us.