Hi John,

We’d argue that WAM is not particularly cheap at current levels. The stock closed Friday at $1.60 versus its last reported NTA of $1.30 at the end of April. In other words, anyone buying WAM today is paying around a 23% premium to the value of the underlying portfolio.

WAM has often traded at a premium, which probably reflects a combination of its long dividend history, strong retail following and effective marketing. However, we would not be comfortable paying such a large premium for exposure to a portfolio that can be bought indirectly at a much lower valuation elsewhere.

The yield is clearly attractive, as you rightly point out, but it is not always simply a pass-through of the returns generated by the underlying portfolio. LICs like WAM can smooth dividends by drawing on profit reserves and capital reserves, meaning part of the dividend can effectively be capital being returned to shareholders, rather than income earned in that period. That helps maintain the headline dividend, but it can also reduce underlying value over time if portfolio performance is not strong enough to support the payout. “Robbing Peter to pay Paul” is probably an apt analogy. This becomes a greater risk if performance remains weak for a sustained period.

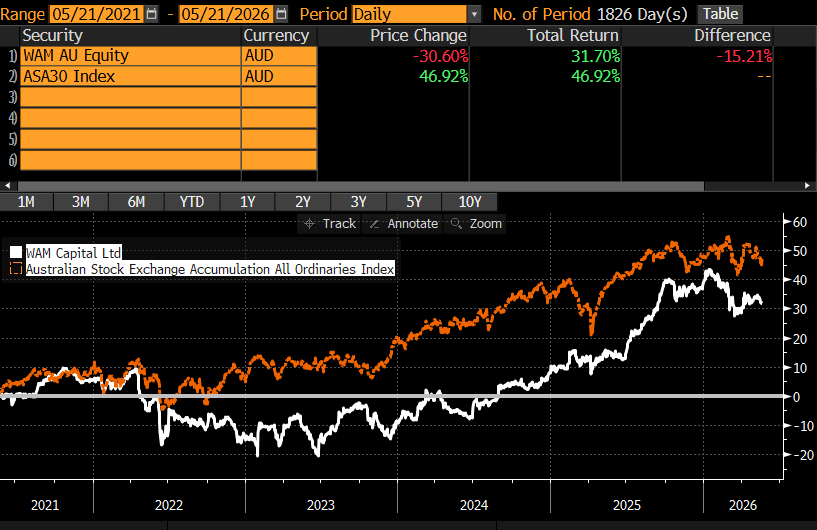

On performance, the chart below compares WAM’s total return, including dividends, with the All Ordinaries Accumulation Index over the past five years. WAM has materially lagged the broader market over that period. So, paying a 23% premium to NTA, plus a 1% annual management fee and a 20% performance fee, does not stack up to us when the LIC has underperformed the market. For context, if you bought WAM five years ago, you would have paid around $2.20 per share, versus today’s price of $1.60. Dividends have offset that capital decline to some extent, but on a total return basis, it has still lagged materially.

We also take issue with how WAM reports performance, or more accurately, how it does not. Its monthly portfolio reports do not provide a clear, consistent table of returns that allows investors to easily compare performance with the index, other funds or other portfolios. We can only assume this is intentional, and we do not like the lack of transparency.

The major risk buying WAM today is that the premium to NTA evaporates. Poor performance often leads LICs to trade at a discount to NTA, not a premium. If that happened, investors could suffer a double hit: weaker portfolio performance and a de-rating in the share price relative to NTA.

In short, while the dividend looks attractive on the surface, we think the risks are meaningful. At current levels, WAM looks expensive, the underlying performance has been poor, the fee structure is high, and the premium to NTA leaves little margin for error.