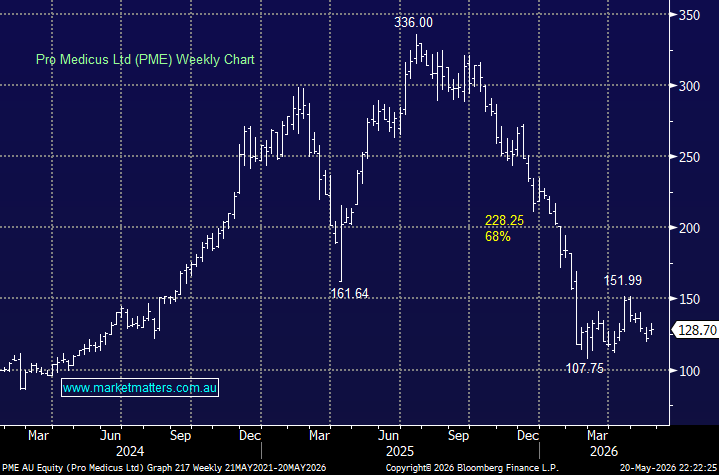

Pro Medicus is a high-margin Australian healthcare technology company that provides imaging software and cloud-based radiology platforms to major hospitals globally, benefiting from the structural digitisation of medical imaging and AI-driven healthcare workflows – a mouthful, but effectively it’s a software company, sitting in the healthcare sector. The market had a love affair with Pro Medicus through 2024 and early 2025, propelling the stock above $300, taking its valuation well above 200x, a vulnerable place to be as bonds fell and the AI Disruption Trade surfaced. The companies continued to deliver with revenue set to increase by ~60% between FY25 and FY27. The problem has been all around valuation contraction.

In simple terms, it’s still a $13.5bn company that only made $169mn in the first half of FY26. We believe this remains one of the best software businesses on the ASX, ~70% EBIT margins, zero debt, compounding contract wins into the world’s largest health systems, and a CEO projecting $1bn revenue within five years. The stock is still not cheap in traditional terms, trading on 80x, but the quality premium is starting to look more justified relative to the price, assuming the contract wins continue to flow – this week they secured a $90mn contract win with Beth Israel Lahey Health to deploy its cloud-based Visage 7 platform.

The AI take is important here, but we feel that AI is likely to enhance Pro Medicus rather than disrupt it, at least over the next decade. Visage sits deep inside major hospital networks as mission-critical infrastructure with enormous switching costs, making it highly unlikely customers abandon a proven platform mid-contract to trial an emerging AI competitor. If anything, the proliferation of AI diagnostic tools arguably strengthens Pro Medicus’ position, because hospitals will increasingly need enterprise-grade imaging platforms capable of integrating, managing and deploying those applications at scale. There are risks from AI, but it looks more long-term than immediate, although AI development is no slow game!

With bond yields capturing the headlines its hard to know when valuation contraction towards high growth stocks will end, but PME is a quality business doing everything right. We could justify starting to accumulate now, but a test of major psychological support ~$100 wouldn’t surprise.

- We especially like the risk-reward toward Pro Medicus around the $100 area – one to watch.

MM is cautiously bullish towards PME around $130, but would leave room to average ~$100

Add To Hit List