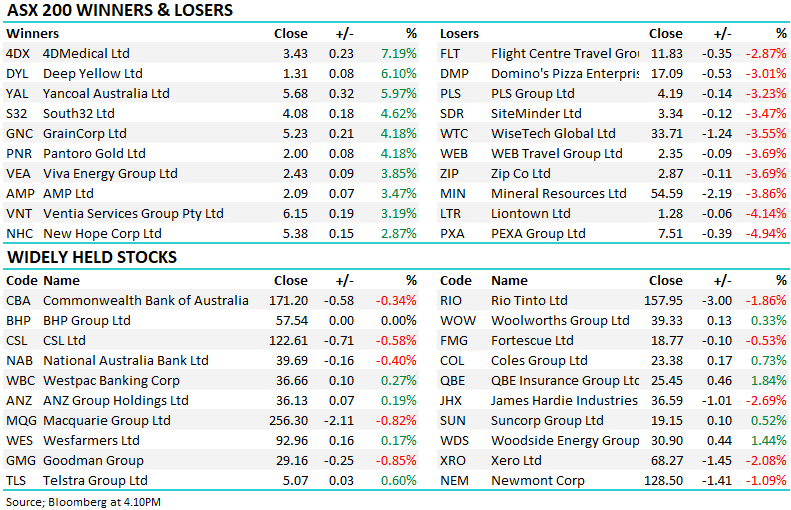

SiteMinder is a global hotel software platform that helps accommodation providers manage room bookings, pricing and online distribution across channels like Booking.com, Expedia and Airbnb. The company makes money through recurring SaaS subscription fees and transaction-based revenue tied to hotel bookings processed through its platform – therein lieth the problem, it sits right in the middle of the “AI Disruption Trade” having been rerated significantly lower along with many in the same growth sector, while at the same time revenue for this $750mn business is set to increase more than 50% over 2-years to ~$340mn in FY27 as it executes well.

We last looked at SDR here, and it’s continued to slide, not helped by the US-Iran war and rising rates starting to weigh on travel appetite. At current levels, the market appears to be pricing a very cautious outlook for this growth company that is still growing nicely, operating in a structurally expanding industry, and retaining a meaningful competitive advantage.

Management has guided to improved profitability through FY26, while analyst consensus currently expects the business to become meaningfully profitable during FY27. The important evolution is that SiteMinder is no longer a “burning cash” SaaS story. The focus has shifted toward how quickly operating leverage can scale as revenue grows, transaction volumes increase, and the Smart Platform strategy matures. While fresh 2026 lows wouldn’t surprise we believe the next ~30% move is far more likely on the upside.

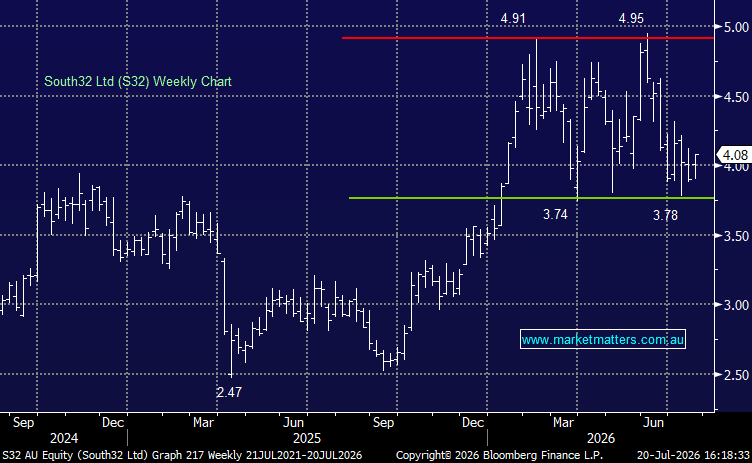

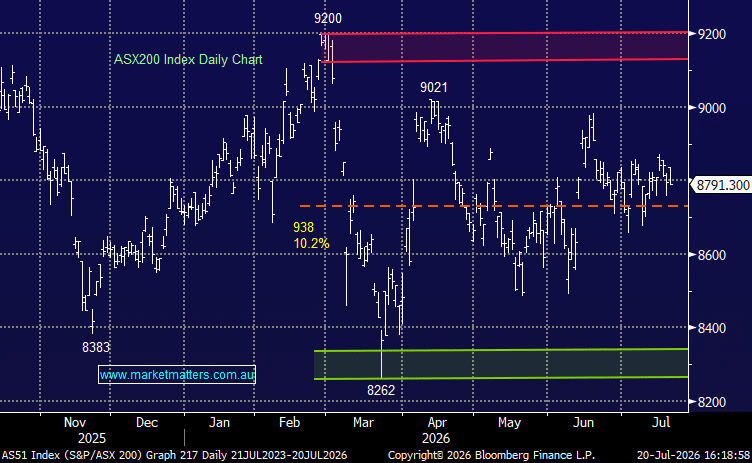

- We can see SDR rotating between $2.50 and $3.50 until the impacts of AI show their hand – MM owns SiteMinder in the Emerging Companies Portfolio.

MM is long and bullish SDR around $2.60

Add To Hit List