DBI +3%: announced FY26/27 distribution guidance of 28.62c per stapled security, an 8.5% uplift on the prior year’s guidance of 26.375c. Importantly, the company also reaffirmed its longer-term target of growing distributions by 3-7% p.a. for the foreseeable future.

- FY26/27 distribution guidance: 28.62c per stapled security, to be paid in quarterly distributions.

- Growth: represents an 8.5% increase on FY25/26 distribution guidance of 26.375c.

- Distribution growth target reaffirmed: DBI continues to target 3-7% distribution growth p.a. for the foreseeable future.

- Terminal Infrastructure Charge: expected to be around $4.02/t for FY26/27, up ~8.1% year-on-year.

DBI’s revenue is supported by long-term infrastructure-style contracts, with the Terminal Infrastructure Charge linked to contracted capacity and benefiting from CPI-linked escalation. The latest TIC increase to around $4.02/t, up more than 8%, reinforces the point that DBI has a genuine inflation-linked cash flow profile.

The 8.5% lift in distribution guidance is above the company’s stated 3-7% target range, while the reaffirmation of that longer-term growth target provides confidence that DBI remains committed to delivering rising income to investors.

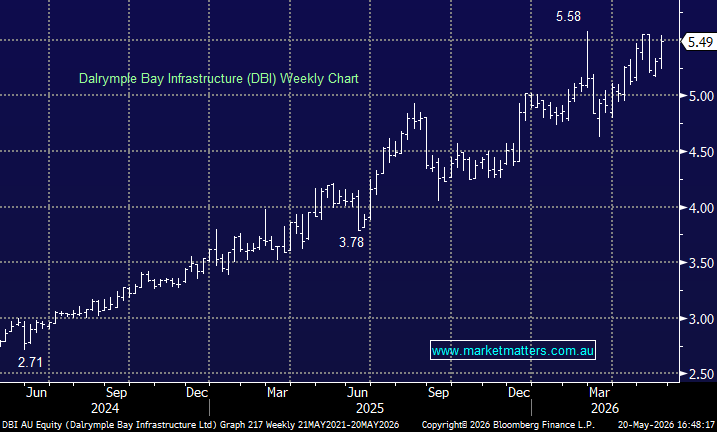

This update reinforces our positive view on DBI. The stock offers an attractive combination of infrastructure-style cash flows, CPI-linked price escalation, growing distributions and a solid yield profile. While the coal exposure will always be a key debate, the underlying income characteristics remain compelling. In a market where investors should be placing a higher value on reliable cash flow, we continue to see DBI as one of the better income exposures on the ASX.

MM remains long & bullish DBI

Add To Hit List