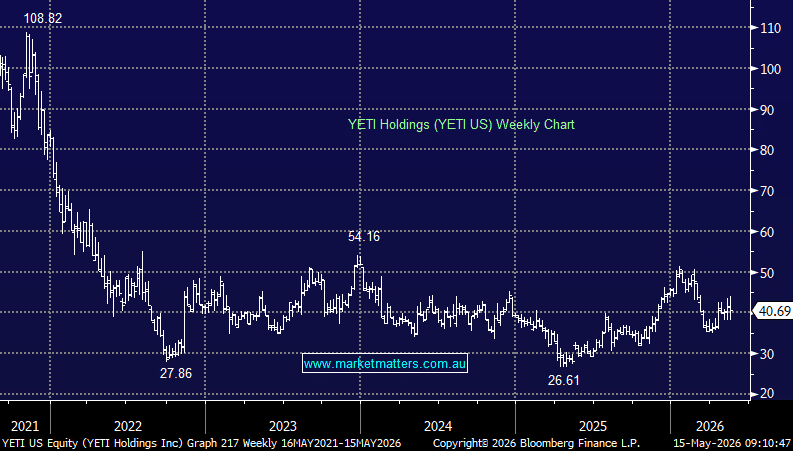

YETI delivered a solid 1Q result overnight and raised FY26 guidance. The stock opened up over 15% higher, before closing up ‘only’ 6%. The outdoor lifestyle brand continues to show decent pricing power and consumer relevance across its core categories of drinkware, coolers and equipment, while the wholesale channel was the standout, suggesting retailers are restocking and/or giving more shelf space to new products. The offset was softer direct-to-consumer momentum, some international softness and the ongoing risk that tariffs and a weaker US consumer environment start to bite later in the year.

1Q Highlights:

- Adjusted EPS: 26cahead of the 18c expected.

- Sales: $380.4m, up +8.3% year-on-year and ahead of the $374.6m expected.

- Wholesale sales: $183.6m, up +19%, well ahead of the $165.8m expected.

- Direct-to-consumer sales: $196.8m, up just +0.3%, below the $207.6m expected.

- Coolers & Equipment sales: $156.1m, up +11%, ahead of the $153.6m expected.

- Drinkware sales: $216.9m, up +5.5%, ahead of the $214.8m expected.

- Adjusted gross margin: 55.3%, down from 57.3% last year but ahead of the 54.1% expected.

- Increased share buyback program to $500m.

YETI now expects FY26 adjusted EPS of $2.83 to $2.89, up from $2.77 to $2.83 previously and mildly ahead of the $2.80 consensus estimate. The company also lifted its adjusted operating margin outlook to around 14.6%, from 14.4%, while raising the lower end of its sales growth guidance to 7% to 8%, from 6% to 8%.

The wholesale strength points to robust sales growth which suggests healthy consumer appetite, shelf-space gains from new products and possibly some inventory catch-up after sell-through had been running ahead of sell-in. In simple terms, retailers appear to really like the brand.

The direct-to-consumer result was more mixed, with sales up just +0.3% and below expectations. Management called out cautious ordering from corporate partners as a drag, though broader DTC demand across Drinkware and Coolers & Equipment remained supportive.

There are still a few things to watch. Tariffs and a potentially softer US consumer as risks, which makes sense for a premium discretionary brand. Margins were better than feared in the quarter, but gross margin was still down year-on-year, and prolonged tariff pressure could make the FY26 margin upgrade harder to deliver. We own YETI in the International Equities Portfolio.

MM remains bullish YETI US ~$US40

Add To Hit List