Hi,

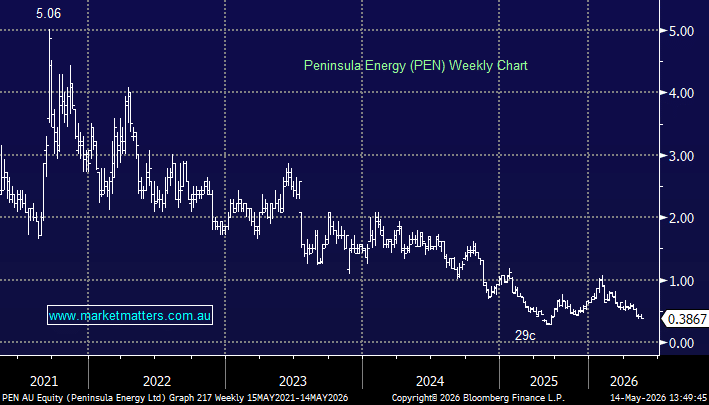

Peninsula Energy Limited (ASX:PEN) went into a trading halt this week while it completes a capital raising, with Washington H. Soul Pattinson emerging as the key backer through two separate commitments. (we own SOL in the Income Portfolio).

- Soul Patts (ASX:SOL) has committed $14.4 million to the equity raising alongside a $30 million convertible note facility — providing PEN with a combined $44.4 million funding package from one of Australia’s most respected long-term investors.

The key detail is the convertible note conversion price of $0.35 per share, modestly below PEN’s last traded price of $0.39 and an important reference point for where SOL sees value. Soul Patts is known for taking long-term positions in businesses at critical inflection points rather than speculative short-term trades. We believe its support materially strengthens confidence in the raising and significantly improves Peninsula’s funding position as it continues ramping up the Lance Project into a strong uranium price environment.

In simple terms, PEN is expected to emerge from the halt with a stronger balance sheet, institutional backing and improved financial flexibility — with the $0.35 conversion level now a key valuation marker for the market.

- PEN is speculative small-cap uranium miner whose capital raise is specifically designed to fund PEN through the FY26 loss year — giving it the balance sheet runway to reach FY27 profitability without another dilutive raise.

Operational execution and funding have been two areas PEN has struggled. While we are not close to this deal, SOL does a lot of DD before making these sorts of investments, and that gives us some confidence, although the mix of funding, skewed more on the debt side, shows that SOL would rather have the majority of it’s investment higher up the capital structure – sensible for them, but does highlight the risks they still see in the development from here. It certainly remains a very high risk way of playing the Uranium thematic, and we don’t have any plans to buy into PEN for now.