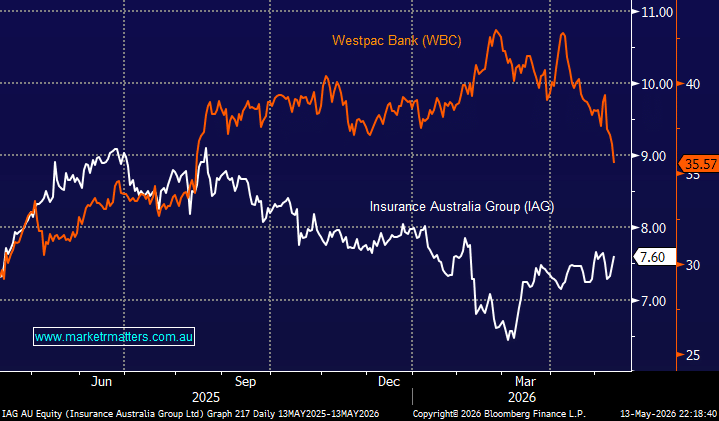

We’ve all heard about the banks over the last 24-hours but the other heavyweight financial sector, the insurers, has largely flown under the radar. Over the years the banks have been retail investors go too for fully franked yield but the insurers are now arguably more attractive, e.g. Westpac’s projected yield of ~4.5% compares to Insurance Australia Group (ASX: IAG) ~4.5%, QBE Insurance (ASX: QBE) ~5% (part-franked) and Suncorp (ASX: SUN) ~5.1%, with all bar QBE fully franked.

The bank selling logic is straightforward: fewer investment property transactions ultimately mean weaker mortgage growth, slower loan book expansion, lower margins and anaemic earnings growth. At the same time, the sector is already grappling with rising provisions and uncertainty around further RBA tightening, highlighted by CBA yesterday. The Budget simply added a structural headwind to an already challenging backdrop for the influential sector. However, the read-through for insurers is more constructive. Higher inflation supports premium growth, rising property market uncertainty potentially increases demand for insurance products, and elevated interest rates continue to boost investment income from insurers’ large fixed-income portfolios.

We discussed Insurance Australia Group (IAG) in mid-April Here, and we like the thematic backdrop for this sector.

- We believe Australian insurance stocks will outperform the banks through 2026 – MM owns QBE in our Active Growth Portfolio and SUN in our Active Income Portfolio.