While QBE and IAG share many of the same AI cost-reduction opportunities, the stories are meaningfully different in scale and focus. QBE is a global operation spanning 20-plus countries, meaning its AI opportunity is vast but complex, requiring execution across multiple regulatory environments and legacy technology stacks. IAG by contrast is predominantly an Australian and New Zealand business — simpler in structure, more domestically concentrated, and arguably better placed to move faster on AI integration given the lower complexity of rolling it out across a single regulatory framework.

Where IAG’s opportunity is most compelling is in its personal lines book, home and motor insurance, which generate enormous volumes of relatively standardised claims that are ideal for AI automation. The NRMA and CGU brands collectively process hundreds of thousands of claims annually, and even modest improvements in straight-through processing rates could deliver material cost savings. IAG has also been more vocal than QBE in flagging AI as a strategic priority in recent results, signalling management intent that the market is yet to fully price, i.e. IAG offers a clean/fast domestic runway with a relatively straightforward path to demonstrable savings within the next two to three years.

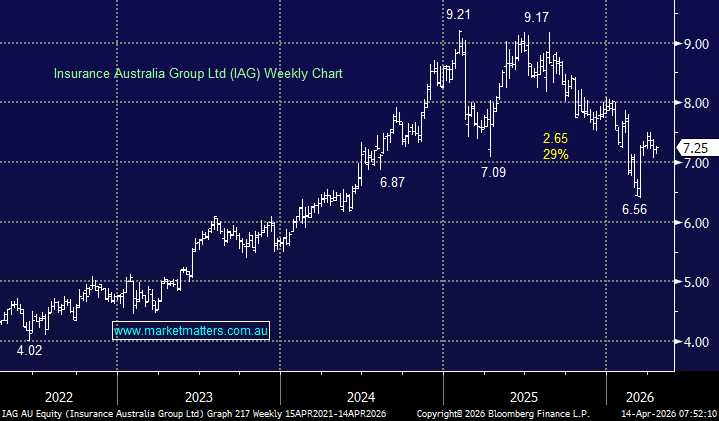

- We like IAG and it has lagged QBE – a recovery back toward $9 looks likely, or ~20% higher.

MM is bullish towards IAG around $7.25

Add To Hit List