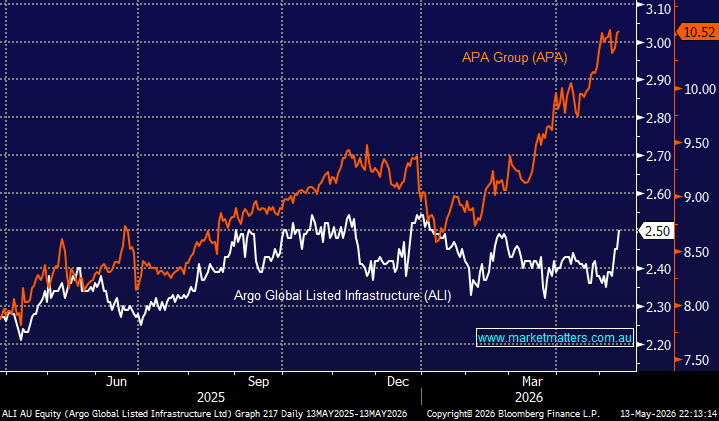

We discussed this subject at length yesterday focusing on Argo Global Listed Infrastructure (ALI) – Here.

Infrastructure ticks most of the boxes a post-Budget income investor should be looking for, real assets providing essential services, regulated or contracted revenues, built-in inflation linkage, and defensive cash flows that sit in a fundamentally different earnings profile to the cyclical parts of the equity market. In a world of sticky inflation, elevated rates, Iran war geopolitical uncertainty, and a CGT regime that now rewards being paid along the way over capital appreciation, that combination has never been more relevant. The thematic backdrop adds further appeal — power demand is accelerating through electrification, AI data centre buildout, and industrial reshoring, while debt-constrained governments globally are increasingly reliant on private capital to fund new infrastructure, creating a structural pipeline of privatisations, asset redevelopments, and new projects.

Argo Global Listed Infrastructure ETF (ASX: ALI): distils all of that into a single ASX-traded vehicle managed by Cohen & Steers, a US-based specialist infrastructure manager overseeing more than US$100 billion, delivering a 6.0% income stream (incl franking), global diversification beyond the ASX’s bank and resources concentration, and a current 9% discount to net asset value that provides a margin of safety.

Of course, it’s not without risk with bond yield sensitivity, currency exposure, and a 1.2% fee, which is quite high, but for income investors seeking inflation protection, geographic diversification, and predictable cash flow in the current environment, we like ALI and have added it to the MM Hitlist.

APA Group (ASX: APA): has been a top performer through 2026, advancing +17%, and we last talked about the utility Here, seeing no reason to “grab” profits from our position in Australia’s largest natural gas infrastructure business – MM owns APA in our Active Growth Portfolio and Active Income Portfolio.

Atlas Arteria (ASX: ALX): is currently in the midst of a takeover, illustrating that private markets still see deep-seated value in infrastructure. We discussed the bid 2-weeks ago Here.

- We like the infrastructure sector through 2026/7 and can see ourselves increasing our exposure across the MM portfolios.