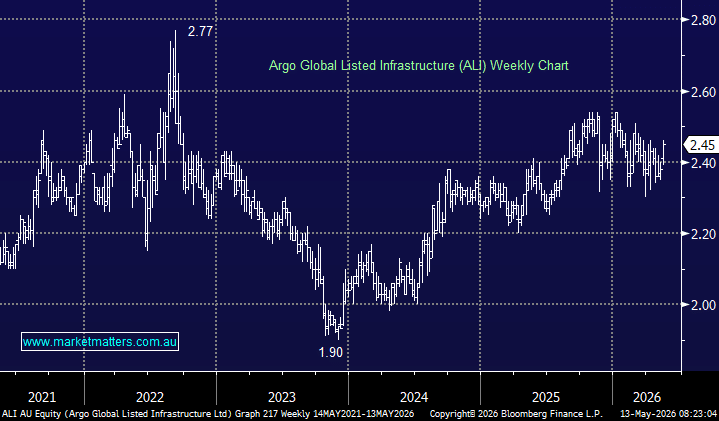

Argo is currently doing the rounds presenting on their approach, and the presentation released to the market on Monday had some good insight into Infrastructure as an asset class for income focussed investors. This is not new news to MM – we like infrastructure, and have exposure to it, but they did a good job of reinforcing the point.

The attraction of infrastructure is pretty straightforward: these are real assets that typically provide essential services, often with regulated or contracted revenue, inflation linkage and relatively defensive cash flows. In a market still dealing with volatile inflation, elevated rates, geopolitical risks and uncertainty around energy prices, that combination has even more appeal. Infrastructure assets are not risk-free, but they tend to sit in a useful part of the market for investors seeking more predictable cash flows. Utilities, toll roads, airports, ports, railways, communications towers, data centres and midstream energy assets are all linked to services the economy needs to function. That gives the sector a different earnings profile to more cyclical parts of the equity market.

We also like the thematic backdrop. Power demand is accelerating, helped by electrification, reshoring, industrial policy and the build-out of AI/data centre infrastructure. At the same time, governments globally are constrained by debt levels, meaning private capital will need to play a larger role in funding new infrastructure. Argo highlights a large infrastructure funding shortfall, creating investment opportunities through privatisations, redevelopment of legacy assets, new projects, IPOs and listed companies expanding their asset bases.

Specifically for Argo Global Listed Infrastructure (ASX: ALI), it gives investors diversified exposure to global listed infrastructure through a single ASX-listed vehicle, with the added benefit of a franked income stream (6.0% inclusive of franking)

The local market is heavily skewed toward banks and resources, while global listed infrastructure provides exposure to different sectors, geographies and cash-flow drivers. When thinking about portfolio construction for income, it’s important to have diversification of income streams, not just relying heavily on the major banks for franked dividends.

The other point is valuation. Infrastructure performed well in 2025 and has started 2026 strongly, but the broader sector still looks reasonably attractive relative to global equities – a point Argo made in their presentation. Valuation is always important, and more so when investing in parts of the market that typically offer lower growth – overpaying for yield is dangerous.

There are of course risks. Higher bond yields can pressure infrastructure valuations, currency moves can impact returns given the global nature of holdings, and listed infrastructure will still move with equity markets during risk-off periods. Some assets, particularly airports and transport-linked infrastructure, also have economic sensitivity. However, we think the broader asset class remains well placed, especially for investors looking for income with some growth and inflation protection.

ALI is also trading at a ~9% discount to asset value which can be normal for LIC’s (Argo itself is trading ~17% below NTA), however we do think about infrastructure slightly differently to a large cap equity portfolio such as ARG. It’s also worth highlighting that ALI is fairly small ($483m NTA), and their fee structure of 1.2% is a lot higher than their main LIC, but this is due to the appointment of an external portfolio manager, US based Cohen & Steers, who are specialists in infrastructure (managing over $US100bn).

- Overall, we like infrastructure and have exposure to it, but not through an LIC structure such as ALI. That said, we think it could be a useful structure to broaden out our exposure more into North American utilities, energy and rail infrastructure over time. We have added ALI to the Hitlist.

MM is positive on ALI ~$2.45

Add To Hit List