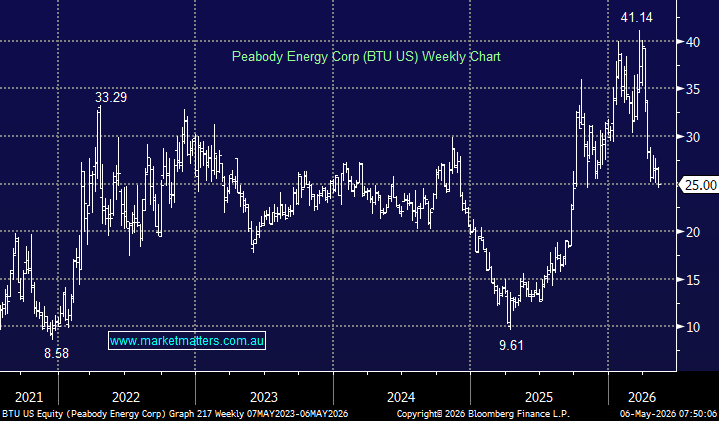

A soft March-quarter result confirmed by Peabody overnight, with the market focusing on a sizeable earnings (EBITDA) miss and ongoing delays at Centurion. The key issue remains execution at Centurion, Peabody’s metallurgical coal growth asset in Queensland, where commissioning issues constrained production. Management says the problems are now resolved, with ramp-up expected through the June quarter and full longwall production rates targeted in the second half. Importantly, this was not new news, with BTU having warned of this in early April (discussed here at the time). Still, shares were down another 5.7% overnight.

1Q Highlights

- Revenue: US$973.3m, up 3.9% YoY, slightly below consensus of US$977.7m.

- Adjusted EBITDA: US$82.5m, down 43% YoY, well below consensus of US$131.6m.

- Operating result: Operating loss of US$44.2m, versus expectations for a US$23.7m profit.

- Guidance: Peabody lifted priced volume expectations across Seaborne Thermal, Seaborne Metallurgical and Powder River Basin, while leaving total volume guidance largely unchanged.

The positives were in thermal coal, where strong demand and higher realised pricing helped offset some of the operational weakness, while the increased priced volume guidance provides better earnings visibility. Still, the quarter was messy, and the EBITDA miss highlights that Peabody remains highly exposed to operational delivery and commodity-price volatility. We think the investment case is now increasingly tied to Centurion ramping cleanly in the second half – if it does, earnings should improve materially.

- While we’re frustrated with this holding, given it briefly traded to our $US40 target late in March, we’ll stay patient, looking for better operational performance in QLD.

MM remains long & cautiously bullish BTU ~$US25

Add To Hit List