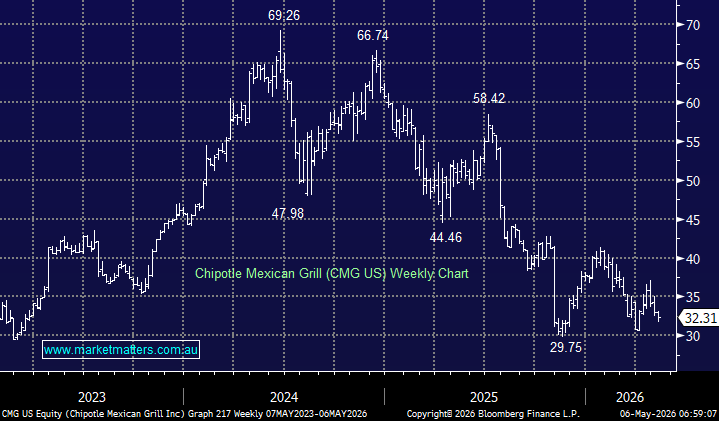

Chipotle’s 1Q result released on the 30th April should be good enough to steady the ship, with comparable sales coming in ahead of low expectations and April trends showing some early improvement. The stock had already been de-rated meaningfully, so while the numbers were not spectacular in absolute terms, they were better than feared.

1Q Highlights:

- Comparable sales rose +0.5%, ahead of consensus expectations for a -0.94% decline, and an improvement on the -0.4% fall recorded in the prior corresponding period.

- Revenue increased +7.4% YoY to US$3.09bn, slightly ahead of expectations for US$3.07bn, helped by store growth and better-than-expected comparable sales.

- Adjusted EPS came in at US24c, in line with consensus, but down from US29c last year, highlighting that the top-line improvement is not yet translating into earnings growth, given margin compression.

- Operating margin fell to 12.9%, down from 16.7% a year ago, though broadly in line with expectations of 13%.

- Restaurant-level operating margin was 23.3%, down from 26.2% last year, reflecting cost pressures and a less favourable sales mix.

- New restaurant openings were light, with 49 new restaurants added during the quarter versus expectations for 64, and down 14% YoY.

- Total restaurants reached 4,090 at period end, slightly below expectations for 4,104, though still up 1.2% QoQ.

- Average restaurant sales were US$3.09m, down 2.9% YoY, but marginally ahead of expectations for US$3.08m.

They left FY guidance unchanged, with management still expecting comparable sales to be around flat for the year, versus consensus looking for +0.89%. New restaurant guidance was also retained at 350–370 openings, broadly in line with consensus expectations of 356.

We own Chipotle in the International Equities Portfolio, and we continue to view it as one of the higher-quality global restaurant operators, with a long store rollout opportunity, strong brand loyalty and attractive unit economics. That said, after a softer growth patch, the market will want more evidence that same-store sales momentum is returning before paying up aggressively again.

- Only some minor (positive) broker revisions after the result – consensus price target $US43.79 with 28 buys, 11 holds and 1 sell.

MM remains cautiously bullish CMG US ~$US32

Add To Hit List