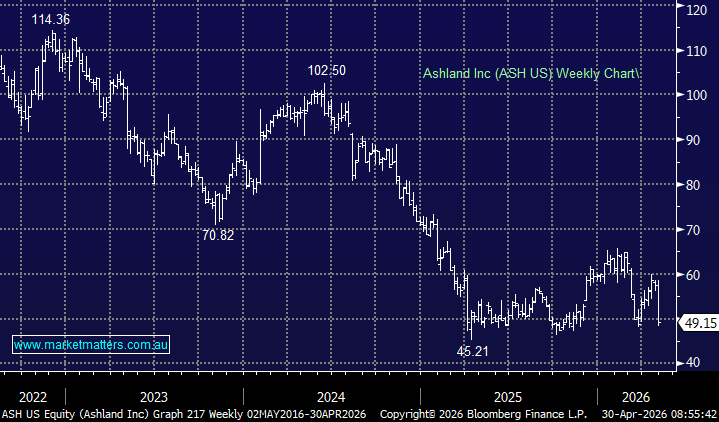

Ashland’s quarterly update overnight was disappointing, with earnings per share coming in lower than expected and the company trimming FY26 guidance. Shares traded down ~13%.

1Q Highlights:

- Sales $482 million vs $484 million est.

- EPS US91c vs US95c est.

- FY26 EBITDA guidance: US$385–400m (previously US$400–420m)

Sales were broadly in line, but guidance was softer. The tempering of guidance was mainly tied to slower-than-expected productivity at the Hopewell HEC site, softer energy-related demand linked to the Middle East conflict, and weaker EV-driven demand for BDO-based derivatives. That said, the result was not all bad. Life Sciences remained steady, supported by pharma applications, while Personal Care delivered double-digit growth.

- Ashland remains a quality specialty ingredients business, but the stock will likely struggle until management shows the Hopewell ramp is back on track and margins stabilise.

MM remains positive on ASH despite lower guidance

Add To Hit List