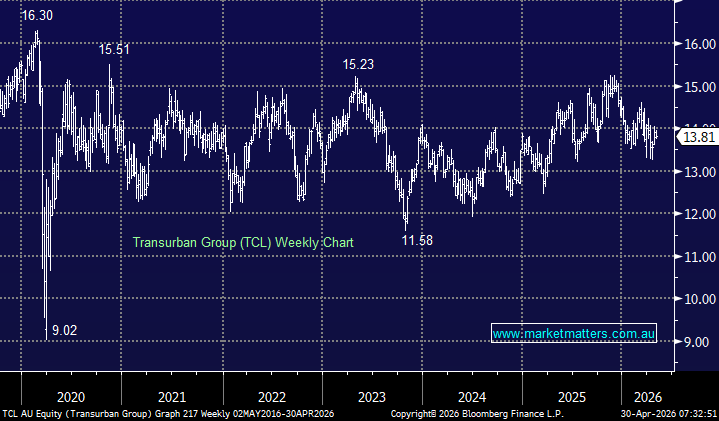

Transurban (TCL) has been an investor favourite over the years but it has traded sideways since COVID while only delivering a ~4.6% unfranked yield. The Toll Road Operator has been a beneficiary of the safety bid over recent years, but its hard to get excited about this large infrastructure company around $14, although the stock is trading on the cheaper side of its historical valuation.

TCL is the quintessential infrastructure asset, high-quality, inflation-linked cash flows, monopoly toll roads and long-dated concessions, making it a natural target for private capital. However, despite trading below pre-COVID highs, several factors make a full takeover highly unlikely. First, size is the biggest hurdle. With a market cap of ~$44bn, any deal would rank among the largest in Australian history, nearly double the Sydney Airport privatisation. Second, the register is already dominated by long-term infrastructure investors (including super funds and sovereign wealth funds), limiting the pool of logical buyers. Third, TCL’s complex web of concessions across multiple jurisdictions creates significant regulatory and approval risk.

TCL ticks every box as a “dream” infrastructure asset but we believe a full takeover remains unlikely.

- We see no reason to buy TCL unless we want to skew MM portfolios more defensively.

MM remains neutral towards TCL

Add To Hit List