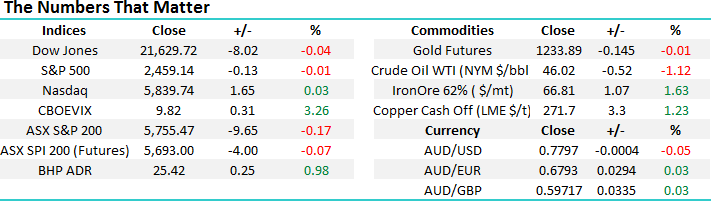

Are 3 “go to” stocks showing signs of cracking?

A disappointing performance from the ASX200 yesterday closing mildly lower and unfortunately ignoring the solid gains from US indices on Friday night which again made fresh all-time highs. Our market has felt on hold over recent weeks as the combination of school holidays and pending news from the banking regulator around capital requirements has been more than adequate to keep many investors on the sidelines. The below simple statistics put things in perspective:

1. The ASX200 has traded in a relatively tight 207-point range since the 18th of May.

2. The average gain for July since the GFC is 4% but so far, this July we are up only 0.6%.

3. The smallest monthly range in 2017 is 160-points, with an average of 213-points but to-date this month we have only traded in a 127-point range.

With only 10-trading days remaining this July the strong implication from these facts is a break of the current 5629-5836 trading range should occur shortly and follow through for at least 50-points. Our “gut feel” is we will get a relief rally in the dominant banking sector following banking regulators announcement – hence the move on the index will be up.

ASX200 Monthly Chart

Following strong gains by the metals overnight today feels likely to be again all about the banks as BHP is implying resource stocks should remain strong. Iron Ore prices should do OK in Asia today after Rio Tinto has this morning cut their production numbers by around 10mtpa.

BHP traded in the US Monthly Chart

US Stocks

Last night US equities were quiet ahead of earnings with the healthcare and financials weak, similar to the Australian market yesterday. There is no change to our current view, we are targeting fresh all-time highs for the NASDAQ around 6000 / 2.5% higher before a decent correction to test early July lows.

US NASDAQ Weekly Chart

European Stocks

The Euro Stoxx 50 is very aligned with the NASDAQ targeting a break over 3700 prior to a decent correction. The key question is “if” the US and European stocks can make these anticipated fresh 2017 highs will the local ASX200 finally manage to eke out some gains.

Euro Stoxx 50 Weekly Chart

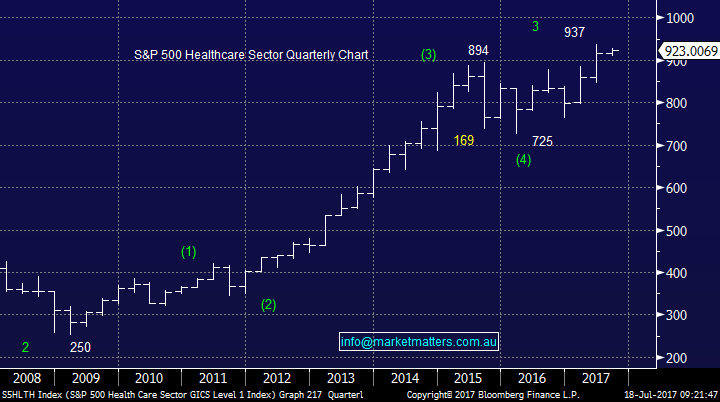

The ASX200 is sitting 200-points / 3.4% below its high of May 1st and while there has been the expected weakness from the local banks its other areas of the market, which have been strong for literally years that have caught our eye as they start to lose their lustre – we have looked at 3 examples today. All 3 companies are quality businesses but there always remains the question “what price should we pay for the stock”.

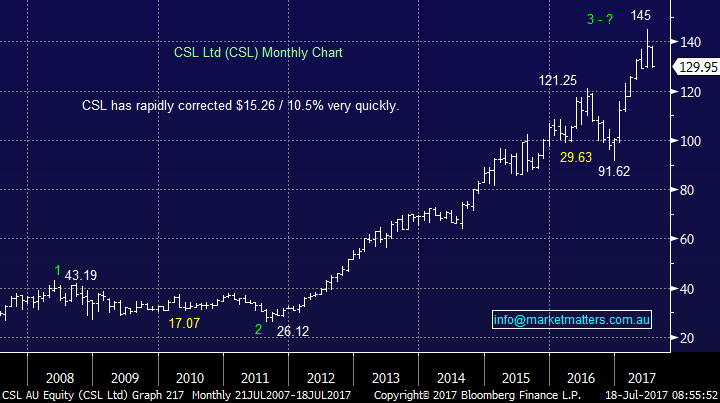

1 CSL Ltd (CSL) $129.95

CSL has been an amazing performer for many years but when the stock surges over 50% this calendar year we have to question whether value remains. Over recent weeks CSL has rapidly corrected ~10% but it’s still trading on Est. P/E for 2017 of 34x earnings which is very much at the rich end of town.

With the US healthcare sector finally reaching our targeted area we are in the minority by going neutral / negative the global healthcare sector. While we may be a touch early with our “sell” opinion we have been bullish for many years so when the sector hits our target we must evolve our outlook accordingly, however unpopular!

CSL and most healthcare stocks has felt a “safe” place to park funds for Australian investors over recent years but the music always ends one day, the story was the same for CBA before it was hammered almost 30% in 2015. We continue to believe we will be able to buy CSL well below $100 in the next 2 years.

S&P500 Healthcare Sector Quarterly Chart

CSL Ltd Monthly Chart

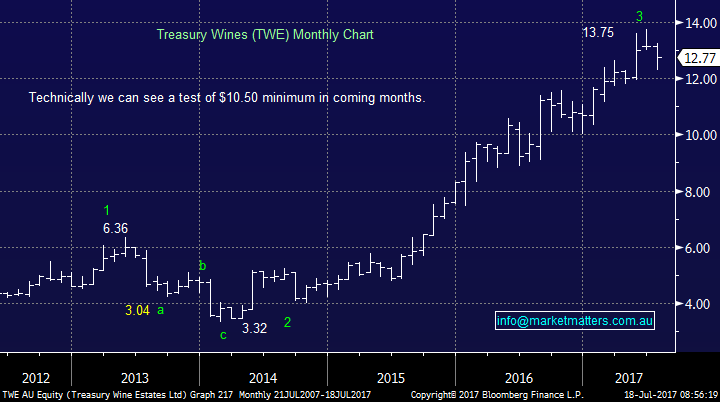

2 Treasury Wines (TWE) $12.77

TWE has enjoyed an excellent 3-4 years but the last 2-months has seen some clear profit taking with the stock trading on an Est. P/E of 31.6x for 2017 earnings. Similar to CSL investors have been comfortable allocating monies to TWE in 2017 at least not expecting to get “hammered”, a phrase we have heard a few times this year.

While we don’t have the same conviction as with the healthcare sector our preferred scenario is TWE corrects a further ~15% towards $10.50.

Treasury Wines (TWE) Monthly Chart

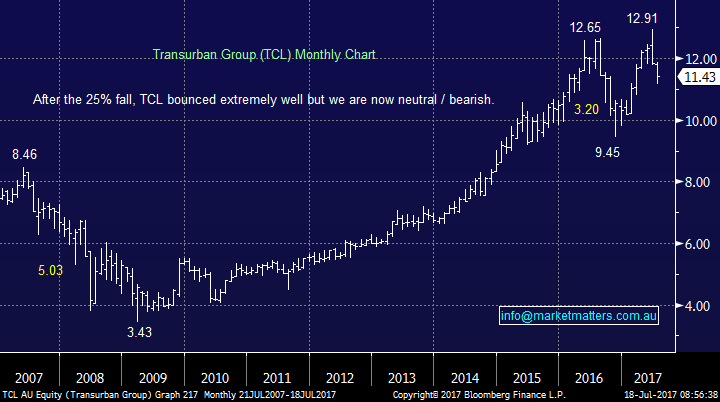

3 Transurban (TCL) $11.43

TCL has rallied – fallen – rallied like a trading stock not the conservative income producer most investors consider the stock to be. The issue is perceived direction of interest rates i.e. higher interest rates is bad news for the TCL share price.

Our view is rates are going higher and the TCL share price is destined to fall back towards at least $10 – investors should not look for safety in numbers!

Transurban (TCL) Monthly Chart

Conclusion (s)

We continue to believe that sector rotation will be a dominant characteristic in 2017 and investors should flexible and open minded. We are now bearish medium term the 3 highlighted “popular” stocks today with the order of negativity TCL, CSL and lastly TWE.

Investing with the crowd has been painful in the past e.g. TLS and CBA and we believe will be again.

**Guidance on Bank Capital Requirements is due out this afternoon**

Overnight Market Matters Wrap

· The US share markets closed with little change overnight as investors sit on the sideline, waiting for further reporting on this current earnings season.

· Iron Ore continues to rally in the seasonal strong period, up 1.63% overnight, following Asia’s 4.79% increase yesterday.

· BHP is expected to outperform the broader market again today, after ending its US session up an equivalent of 0.98% from Australia’s previous close.

· The June SPI Futures is indicating the ASX 200 to open 7 points lower testing the 5748 level this morning.

Disclosure

Market Matters may hold stocks mentioned in this report. Subscribers can view a full list of holdings on the website by clicking here. Positions are updated each Friday.

Disclaimer

All figures contained from sources believed to be accurate. Market Matters does not make any representation of warranty as to the accuracy of the figures and disclaims any liability resulting from any inaccuracy. Prices as at 18/07/2017. 8.00AM.

Reports and other documents published on this website and email (‘Reports’) are authored by Market Matters and the reports represent the views of Market Matters. The MarketMatters Report is based on technical analysis of companies, commodities and the market in general. Technical analysis focuses on interpreting charts and other data to determine what the market sentiment about a particular financial product is, or will be. Unlike fundamental analysis, it does not involve a detailed review of the company’s financial position.

The Reports contain general, as opposed to personal, advice. That means they are prepared for multiple distributions without consideration of your investment objectives, financial situation and needs (‘Personal Circumstances’). Accordingly, any advice given is not a recommendation that a particular course of action is suitable for you and the advice is therefore not to be acted on as investment advice. You must assess whether or not any advice is appropriate for your Personal Circumstances before making any investment decisions. You can either make this assessment yourself, or if you require a personal recommendation, you can seek the assistance of a financial advisor. Market Matters or its author(s) accepts no responsibility for any losses or damages resulting from decisions made from or because of information within this publication. Investing and trading in financial products are always risky, so you should do your own research before buying or selling a financial product.

The Reports are published by Market Matters in good faith based on the facts known to it at the time of their preparation and do not purport to contain all relevant information with respect to the financial products to which they relate. Although the Reports are based on information obtained from sources believed to be reliable, Market Matters does not make any representation or warranty that they are accurate, complete or up to date and Market Matters accepts no obligation to correct or update the information or opinions in the Reports.

If you rely on a Report, you do so at your own risk. Any projections are estimates only and may not be realised in the future. Except to the extent that liability under any law cannot be excluded, Market Matters disclaims liability for all loss or damage arising as a result of any opinion, advice, recommendation, representation or information expressly or impliedly published in or in relation to this report notwithstanding any error or omission including negligence.

To unsubscribe. Click Here