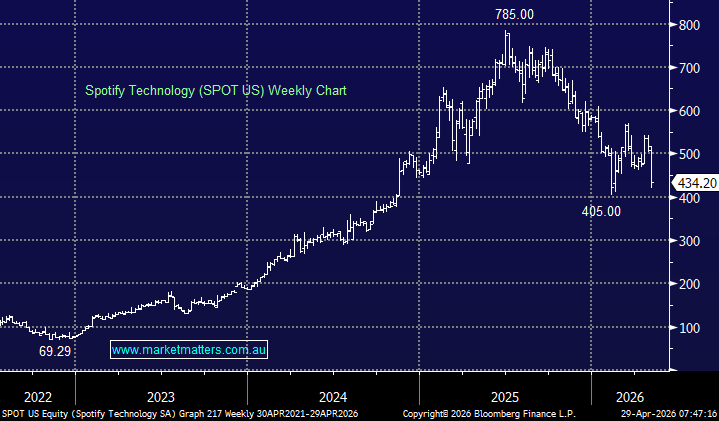

Spotify delivered a solid March quarter result overnight, but as is generally the case, the focus was on guidance, and it was underwhelming. Shares fell ~12%.

We own Spotify in the International Equities Portfolio and continue to like the medium-term story, though the overnight update shows why we’ve retained a smaller ~3% weighting as the monetisation of the huge user base take shape. This was the area within the guidance that underwhelmed.

1Q Highlights:

- Operating income EU715 million, +40% y/y

- Revenue EU4.53 billion, +8.2% y/y, estimate EU4.53 billion

- Premium revenue EU4.15 billion, +9.6% y/y, estimate EU4.11 billion

- Gross margin 33%, estimate 32.8%

- Monthly active users 761 million, +12% y/y, estimate 759.23 million

- Total premium subscribers 293 million, +9.3% y/y, estimate 293.3 million

- Ad-supported MAUs 483 million, +14% y/y, estimate 479.29 million

- EPS EU3.45 vs. EU1.07 y/y

The quarter itself was fine. Revenue was in line with expectations and up +8.2% on last year, while operating income was up +40% year-on-year. Earnings per share were also comfortably ahead of expectations, helped by continued discipline around costs and improving profitability across the platform. Gross margin improved to 33%, slightly ahead of consensus, while monthly active users grew +12% to 761m, also ahead of expectations.

Premium subscribers were broadly in line and up +9.3% year-on-year, which is a reasonable outcome given recent price increases. Importantly, the user base remains very healthy, with ad-supported MAUs up +14%. Management also pointed to better engagement in key markets like the US following the global rollout of a more personalised free experience, with users listening and watching more days per month.

For Q2, they guided to monthly active users of 778 million, which was ~4m ahead of expectations, however profit guidance of EU630 million was around 6.5% light on. Gross margin guidance of 33.1% implies only a very modest step up from the March quarter. That was the disappointment. The key to SPOT’s monetisation strategy is its ability to expand margins over time, and Q2 guidance showed only a modest uplift.

There are a few moving parts here, but the market focused on the new “Streaming 2.0” label deals, including with Universal Music, and whether higher royalty payments cap the upside to margins. AI-generated music is also a concern, and could be starting to take share, or at least influence listening behaviour, which adds another layer of uncertainty. (AI-generated music is music created partly or entirely using artificial intelligence rather than being fully written, played, or produced by humans).

We think AI is more likely to be a double-edged sword than a simple negative for Spotify. On one hand, AI-native music platforms like Suno and Udio, along with larger players such as Google and Amazon, could increase competition and content costs. On the other hand, Spotify’s scale, data advantage and personalisation engine should be powerful tools in improving discovery, engagement and monetisation.

The company has already shown it can use product innovation to increase time spent on the platform, and that remains a key part of our investment case. Advertising remains the weaker part of the business, though this should improve through the second half if macro conditions improve and Spotify continues to build out better ad products. Premium remains the core profit engine, and the fact that subscriber momentum has held up despite price increases is encouraging.

MM’s view is that this result does not break our thesis, but it does imply a lower growth earnings picture in the short term. User growth remains strong, subscriber trends are resilient, pricing power is evident, and profitability is moving in the right direction. However, clearly, the market wanted more confidence around the pace of margin expansion, which today’s guidance did not provide.

The business has moved from a pure growth story to one with genuine earnings leverage, and we think the combination of scale, pricing power, product innovation and improving cost discipline still supports the stock moving forward. That said, the market is right to focus on margins, particularly as label deals, royalties and AI-related investment become more important variables.

- Overall, we still think this is a high-quality growth story, and we’ll likely add to our exposure when we get more clarity around margin improvement.