Hi Dario,

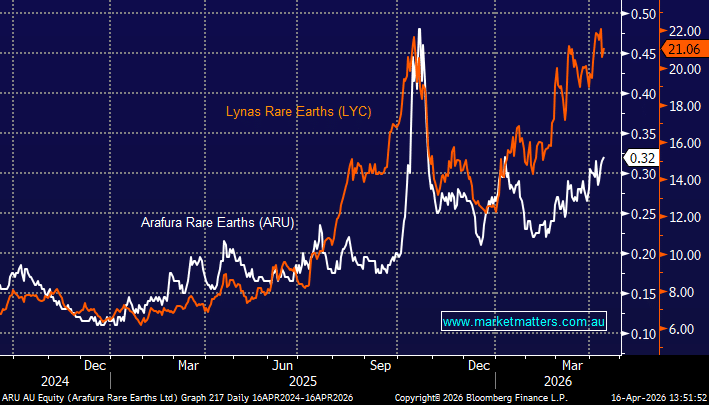

These 2 rare earth stocks are at very different stages of their evolution:

Lynas (LYC): is the mature operator if you want exposure to the rare earth’s thematic with a business that’s actually making money today, it’s the clear choice. The valuation is not cheap, but you’re paying for the only scaled Western producer outside China.

- LYC is estimated to generate $1.1bn of revenue in 2026 and $1.8bn in 2027.

Arafura: is the high-risk junior, but has a solid register and sovereign backing, Gina Rinehart’s anchor investment, and binding offtakes with Hyundai and Siemens Gamesa give it more credibility than most pre-production stories. But it’s a 2029/2030 production story at best, and the US EXIM binding commitment remains the line-in-the-sand catalyst.

- Investors buying ARU today are looking at a ~4 year wait to first revenue in any material sense, and probably 2031-2032 before the project is truly firing.

We prefer LYC over ARU due to the long and potentially uncertain lead time before ARU commences production. These are 2 volatile stocks which we wouldn’t currently consider chasing into strength:

- We see decent risk/reward for LYC ~$18 and ~30c for ARU.